How to Manage Risk in a Small Business

Quick Answer

To manage risk in a small business, start by listing what could realistically go wrong — an injury, a lawsuit, a key person leaving, a data breach, a missed compliance deadline, a fire or flood. Score each one two ways: how likely it is, and how badly it would hurt if it happened. Plotting those two scores on a simple likelihood-by-impact matrix sorts a long worry list into the handful that actually deserve your limited time and money. For each of those, pick one of four responses — avoid it, reduce it, transfer it (usually insurance), or knowingly accept it — then put the control in place, give it an owner and a date, and write down what you did. The required pieces aren't optional: documented OSHA safety practices, anti-harassment and anti-discrimination safeguards, and the records to prove both. Finish by watching a few honest signals — open high-priority risks, incidents and near-misses, whether your compliance items are current — and re-checking the list a couple of times a year and after anything major changes. You don't need a risk department or enterprise software to do this well — you need a short, repeatable habit and a reliable way to document it, which an HR or PEO partner can supply if you don't have one in-house.

Step-by-Step Guide to Managing Risk

- List What Could Go Wrong: Walk the business in your head — or literally walk the floor — and write down what could disrupt it: an injury, a harassment or wrongful-termination claim, losing your one person who knows a critical task, a ransomware attack, a missed renewal, a supplier failing. In a small company this is a conversation and a short list, not a formal audit. The goal is to get the worries out of your head and onto one page, where you can see them.

- Score Each Risk by Likelihood and Impact: Rate every item two ways — how likely it is to happen, and how badly it would hurt if it did — on a simple low/medium/high scale. Multiplying or plotting the two is what turns a scary list into a ranked one. The risk assessment matrix below is the tool for this and takes about an hour for a small business.

- Prioritize the Few That Matter: The point of scoring is to stop trying to fix everything. The high-likelihood, high-impact risks come first; the rare, minor ones can wait or be ignored on purpose. A small business that protects against its top five exposures is far safer than one that owns a thick binder it never acts on.

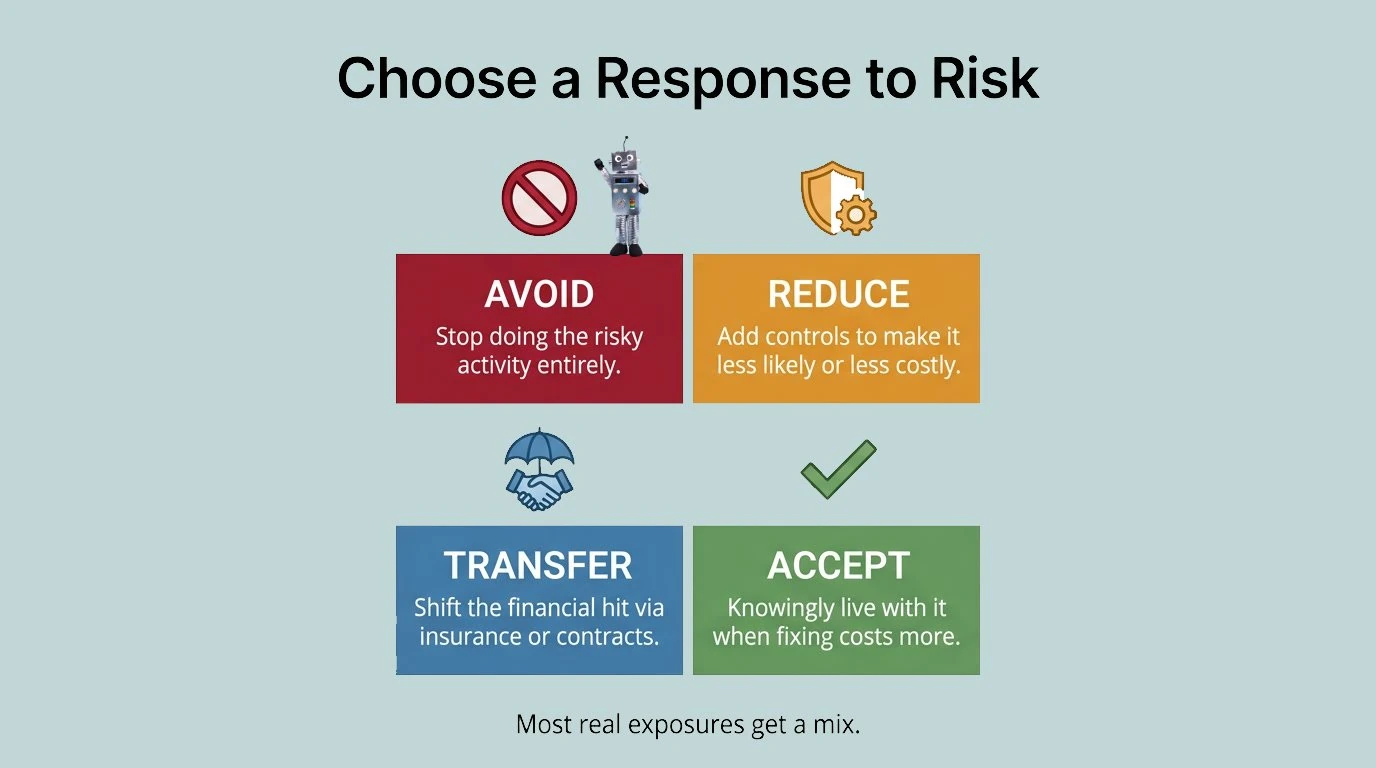

- Choose a Response — Avoid, Reduce, Transfer, or Accept: For each priority risk, decide how you will handle it. Stop doing the risky thing (avoid), put in a control that makes it less likely or less costly (reduce), shift the financial hit to someone else through insurance or a contract (transfer), or knowingly live with it because the cost of fixing it is higher than the risk (accept). Most real exposures get a mix.

- Put the Control in Place: Turn the decision into something concrete — a written procedure, a guard on a machine, an off-site backup, a signed policy, the right insurance limit, a second person cross-trained on the critical task. A response that lives only in your head isn't a control.

- Assign an Owner and a Date: Every priority risk gets one named person responsible and a deadline. In a small business that's often the owner or a manager, but writing it down is what keeps "we should really fix that" from sitting unfixed for two years.

- Document the Risk, the Control, and the Proof: Record each risk, what you decided to do about it, and the evidence it's handled — policy acknowledgments, training completions, certificates, inspection notes, insurance declarations. For anything legally required, if you can't show it was done, in practice it didn't happen.

- Train People on the Controls: A control only works if the people doing the work follow it. Make sure required safety and harassment-prevention training is completed and that everyone knows the procedures that keep your top risks in check. Controls fail quietly when no one was enabled to follow them.

- Monitor a Few Signals and Review on a Schedule: Track a short list of indicators — open high-priority risks, incidents and near-misses, whether compliance items are current — and re-rate the whole list at a set interval (quarterly or twice a year is plenty for most small businesses), plus immediately after any incident or major change. Drop controls that aren't reducing risk and add new controls as the business changes.

How to Manage Risk

In small to medium-sized companies, risk management is less about software and frameworks and more about being deliberate. You won't have a risk officer or a compliance department, so the quality of your protection comes down to a few decisions the owner or manager makes up front — what could actually hurt the business, which of those threats is worth money and attention, who's responsible for each, and how you'll know your exposure went down. Get those right and a small team can be as well-protected as anyone; skip them and risk management becomes a binder no one opens until something goes wrong.

Start by Listing What Could Go Wrong

The most common mistake is buying a solution — a policy, a piece of insurance, a tool — before naming the problem. Before you spend anything, ask what could realistically disrupt or sink the business: the work you do, the people you depend on, the rules you have to follow, the things outside your walls. You already know most of the answers; they're the things that keep you up at night and the near-misses you've waved off. Write them down. Only a real, named risk earns a control, which keeps your limited time and budget pointed at threats that matter instead of the ones that merely feel scary.

Rank by Likelihood and Impact

Not every risk deserves equal attention, and a small business can't afford to act as if it does. Score each one on two axes — how likely it is, and how much damage it would do — and the list sorts itself. A rare event that would barely dent the business sits at the bottom; a likely event that could close your doors goes straight to the top. This is the single most useful habit in small-business risk management, because it tells you where to start and gives you permission to stop worrying about the rest.

Match the Response to the Risk — and Keep It Inexpensive

There are only four things you can do with a risk: avoid it, reduce it, transfer it, or accept it. Avoiding means not doing the risky thing at all; reducing means a control that lowers the odds or the cost; transferring usually means insurance or a contract clause that puts the financial hit on someone else; accepting means deciding, on purpose, that a small risk isn't worth spending on. Small businesses rarely need expensive systems — they need to pick the right one of those four for each top risk and follow through.

The Owner or Manager Is the Risk Program

Risk management that ends when the spreadsheet is filled in rarely protects anything. In a small business there's no separate function to hand this off to — the owner or manager is the bridge between "we identified it" and "it's actually controlled," through assigning owners, checking that controls got built, and revisiting the list on a schedule and after every incident. That follow-through is what turns a list of worries into real protection, and it's the piece that fails in most small companies.

Measure Whether Exposure Actually Dropped

"We made a risk list" tells you someone spent an afternoon; it says nothing about whether the business is safer. Watch that your high-priority risks are actually controlled and owned. Are your incidents and near-misses trending down? Are the required compliance items current and documented? You don't need a dashboard. A short list of the few exposures you're trying to shrink, reviewed a couple of times a year, tells you which controls to keep and which to rebuild.

Risk Management Definition

Risk management is the structured way a business identifies what could go wrong, decides which of those threats is worth acting on, and puts protections in place before problems happen instead of after. For a small company it usually covers legal and compliance exposure, workplace safety, employment practices, finances, day-to-day operations, data security, and reputation. Small businesses manage risk for the same reasons as big ones — to avoid losses that could close the doors and to keep the business running through disruption — but small businesses do it with far fewer people and tools, which makes a simple, repeatable approach essential rather than optional.

The Four Ways to Treat a Risk

- Avoid: Stop doing the activity that creates the risk, or don't start it. The cleanest option when a risk is severe and the activity isn't essential — but often impractical, since most risk comes from work you actually need to do.

- Reduce (Mitigate): Put a control in place that lowers the likelihood, the impact, or both — a safety procedure, a backup, cross-training, a written policy. This is the powerhouse of small-business risk management and where most of your effort goes.

- Transfer: Shift the financial consequences to someone else, usually through insurance (liability, workers' comp, cyber, property) or a contract clause. You still own the risk; you've just made sure a single bad event doesn't come straight out of your pocket.

- Accept: Knowingly decide to live with a risk because it's small or because controlling it would cost more than the value of dealing with it. Acceptance is a legitimate choice — as long as it's deliberate and documented, not just an oversight.

Overview of Related Topics

- Step-by-Step Guide to Managing Risk: A simple process that runs from listing what could go wrong, through scoring and treating the few that matter, to monitoring and review — sized for a team without a risk or compliance department.

- Types of Business Risk: The categories a small company actually faces — compliance and legal, workplace safety, employment practices, financial, operational, cyber and data, and reputational — each with its own likely sources and controls.

- Who Does What: Risk in a small business is carried by a few people — the owner or manager who decides and reinforces, an experienced employee who knows where the operational risks are, an HR or PEO partner who supplies compliance expertise and recordkeeping, and an insurance broker who handles the transfer pieces.

- Compliance Considerations: Federal law requires documented workplace safety practices (OSHA) and prohibits harassment and discrimination (EEOC), with no exemption for small employers — so a small business needs both the controls and effective records.

- Measuring Effectiveness: You don't need a risk analyst. A few simple signals — are the top risks controlled, are incidents dropping, are compliance items current and documented — communicate what's working.

Topics

Types of Business Risk

- Compliance & Legal: Missed filings, expired licenses, wage-and-hour mistakes, and failure to meet mandated training or recordkeeping rules. Often the easiest to overlook and among the most expensive to get wrong.

- Workplace Safety: Injuries, hazardous conditions, and OSHA violations. Carries direct human cost, workers' compensation exposure, and federal penalties — with no headcount exemption for small employers.

- Employment Practices: Harassment, discrimination, wrongful-termination, and retaliation claims. A single claim can cost a small business far more than the policies and training that would have prevented it.

- Financial: Cash-flow gaps, a major customer that doesn't pay, fraud, or underpricing. In a small company there's less cushion, so a financial shock lands harder and faster.

- Operational: A key person leaving, a critical supplier failing, equipment breaking, or a process that only one person understands. The everyday risks that quietly determine whether the work keeps moving.

- Cyber & Data: Ransomware, phishing, lost devices, and data breaches. Attackers increasingly target small businesses precisely because their defenses are thinner.

- Reputational: A bad review cycle, a public mistake, or a customer-data incident. Harder to insure and slower to rebuild, which makes prevention the main lever.

Who Does What

- Owner / Manager: Decides which risks matter, makes the time and budget to control them, and reinforces the program through follow-up. In a small business this one person wears the hats a large company splits across a risk, compliance, and safety team.

- Experienced Employee (Your In-House Expert): Knows where the real operational risks are — the step that breaks, the customer who's difficult, the task only they can do. Capturing that knowledge before they leave is one of the highest-value risk controls.

- HR / PEO Partner: Supplies compliance expertise, ready-made safety and harassment-prevention content, audit-ready recordkeeping, and answers to the "are we required to do this?" questions — the specialist knowledge a small company can't justify hiring full-time.

- Insurance Broker: Handles the transfer side — matching liability, workers' comp, property, and cyber coverage to your actual exposure so a single event doesn't come straight out of the business.

Regulatory & Compliance Considerations

- OSHA Safety Requirements: OSHA requires safe working conditions, documented safety practices, and training for hazardous roles, and the records must be kept. This applies to small employers — there's no headcount exemption, even where penalty reductions exist for small companies.

- Anti-Harassment & Discrimination (EEOC): Federal law prohibits workplace harassment and discrimination, and a growing number of states require harassment-prevention training for even small employers — so written policies, training, and documentation are baseline risk controls, not nice-to-haves.

- Documentation & Recordkeeping: If a control isn't documented, in practice you can't prove it existed. Small businesses are audited and sued too, and clean records — policy acknowledgments, training completions, inspection notes, incident logs — are your defense. This is one of the clearest reasons to lean on an HR partner's tracking.

Measuring Effectiveness

- Are the Top Risks Controlled: Every high-priority risk should have a control in place and a named owner — aim for zero high-priority risks sitting unaddressed.

- Are Incidents Dropping: Injuries, claims, near-misses, and outages, tracked before and after you put controls in. A measurable drop is proof the effort paid off.

- Are Compliance Items Current: Required training, licenses, certifications, and insurance — all current and documented. Aim for 100%, which is realistic with only a small group.

- Did You Survive the Surprises: The real test is whether an event that would have closed an unprepared business became a manageable bad week instead.

Risk Assessment Matrix: A Likelihood-by-Impact Template

A risk assessment matrix is the single most useful tool in small-business risk management. It takes your list of "things that could go wrong" and scores each one on two simple axes — how likely it is to happen, and how badly it would hurt — then plots them on a grid so the priorities sort themselves. It works especially well for a small team: it forces a fast, honest conversation, it produces a one-page picture the owner can act on, and it tells you not just what to worry about but, just as importantly, what you can safely ignore. You can build this whole thing on a single shared page in about an hour.

Step 1: Score Likelihood (1–5)

- 1 — Rare: Hard to imagine it happening; no real history of it.

- 2 — Unlikely: Could happen, but you wouldn't expect it in a typical year.

- 3 — Possible: Happens occasionally to businesses like yours.

- 4 — Likely: You'd expect it at least once in the next year or two.

- 5 — Almost Certain: It's happened before and will again unless something changes.

Step 2: Score Impact (1–5)

- 1 — Negligible: A minor nuisance; absorbed without much notice.

- 2 — Minor: Some cost or disruption, handled within normal operations.

- 3 — Moderate: A real hit — lost time, money, or a customer — that you'd feel.

- 4 — Major: Serious financial, legal, or operational damage; recovery takes effort.

- 5 — Severe: Could threaten the survival of the business.

Step 3: Plot Each Risk on the Matrix

Multiply or plot the two scores. Where a risk lands tells you how urgently to act: the upper-right corner — likely and severe — is where your resources and attention go; the lower-left corner — rare and negligible — is usually a deliberate "accept and move on."

| Likelihood → | ||||||

|---|---|---|---|---|---|---|

| 1 Rare | 2 Unlikely | 3 Possible | 4 Likely | 5 Almost Certain | ||

| ← Impact | 5 Severe | 5 | 10 | 15 | 20 | 25 |

| 4 Major | 4 | 8 | 12 | 16 | 20 | |

| 3 Moderate | 3 | 6 | 9 | 12 | 15 | |

| 2 Minor | 2 | 4 | 6 | 8 | 10 | |

| 1 Negligible | 1 | 2 | 3 | 4 | 5 | |

- Low (1–3): accept & monitor

- Medium (4–9): plan a control

- High (10–15): act soon

- Critical (16–25): act now

Step 4: Turn the Top Risks Into a Risk Register

For everything that lands in the high or critical zone, capture a single line in a simple risk register — a shared spreadsheet works fine: the risk, its likelihood and impact scores, the response you chose (avoid, reduce, transfer, accept), the control you're putting in place, the person who owns it, and a review date. That register becomes the working document of your whole program. Keep it on one page, revisit it at each review, and re-score risks as controls go in or as the business changes — the score on a well-controlled risk should drop over time, and that movement is the clearest proof your risk management is working.

The completed matrix and register also act as evidence: if you're ever audited or facing a claim, a dated record showing you identified a risk, scored it, and acted on it is exactly the kind of documentation that demonstrates a reasonable, good-faith program — keep it on file.

Risk Management Checklist

Use this checklist as the backbone of any risk review — an annual once-over, a new line of business, or a response to something that just went wrong. Adapt it to your business and your industry's rules, but keep every item something you can mark done or not done. None of it requires a big system; a shared document works fine, and an HR or PEO partner can handle the compliance and tracking pieces if you'd rather not.

Identifying Risks

- A written list of what could realistically go wrong, across compliance, safety, employment, financial, operational, cyber, and reputational categories.

- Input gathered from the people closest to the work, not just the owner.

- Past incidents and near-misses reviewed for patterns worth acting on.

- Single points of failure noted — tasks, suppliers, or systems only one person or vendor covers.

Assessing & Prioritizing

- Each risk scored for likelihood and impact.

- Risks plotted on the matrix and sorted into low, medium, high, and critical.

- The handful of high and critical risks agreed on as this cycle's priorities.

- A deliberate "accept" decision recorded for the low risks you're choosing not to act on.

Treating & Controlling

- A response chosen for each priority risk — avoid, reduce, transfer, or accept.

- Required compliance controls confirmed in place (OSHA safety practices, anti-harassment policy and training, any industry requirements).

- Insurance coverage checked against actual exposure, with gaps flagged for your broker.

- Each control assigned a named owner and a due date, captured in the risk register.

- People trained on the procedures that keep the top risks controlled.

Ongoing Monitoring & Compliance

- A review date set — at least once or twice a year, plus after any incident or major change.

- Incidents, claims, and near-misses logged so trends are visible.

- License, certification, and insurance renewal dates tracked, with renewals scheduled before they lapse.

- Records kept audit-ready and organized — the piece an HR or PEO partner can take off your plate.

- Risk scores re-checked so you can see whether controls are actually lowering exposure.

Statistics & Outlook

Managing risk isn't just a big-company concern — it's a mix of legal obligations that apply regardless of headcount and exposures that hit small businesses disproportionately hard. On the compliance side, the numbers are concrete: OSHA's 2025 maximum penalty reached $165,514 for a willful or repeated violation and $16,550 for a serious one, and while the agency expanded penalty reductions for small employers in 2025, none of that waives the underlying duty to provide a safe workplace and keep records (OSHA, osha.gov/penalties). Employment exposure is just as real — the U.S. Equal Employment Opportunity Commission reported securing roughly $660 million for about 17,680 workers in fiscal year 2025 against more than 88,000 discrimination charges filed, with most of that money recovered before cases ever reached court (U.S. EEOC, eeoc.gov).

For a small business, the case for managing risk deliberately is if anything more compelling than for a large one. The Federal Emergency Management Agency has long estimated that around 40% of small businesses never reopen after a disaster, with more failing in the year that follows — a survival gap that comes down largely to whether a business planned for disruption before it arrived (FEMA, ready.gov/business). The good news is that the method is well established and scales down: the internationally recognized ISO 31000 standard lays out a simple, sector-neutral process — identify, assess, treat, then monitor and review — explicitly intended to apply to organizations of any size (ISO, iso.org). A single uninsured lawsuit, one serious safety citation, or one disruption with no continuity plan is a far larger share of a 25-person operation than a 25,000-person one. Small businesses that treat risk management as a simple, repeatable habit — and lean on an HR or PEO partner for the compliance and recordkeeping pieces — get much of the protection of a far larger company without the overhead.

Verified Sources

- Occupational Safety and Health Administration (OSHA) — 2025 maximum penalties reached $165,514 per willful or repeated violation and $16,550 per serious violation; employers must provide a safe workplace and maintain records regardless of size. (osha.gov)

- U.S. Equal Employment Opportunity Commission (EEOC) — Secured approximately $660 million for about 17,680 workers in FY 2025 against more than 88,000 discrimination charges filed, the bulk recovered before litigation. (eeoc.gov)

- Federal Emergency Management Agency (FEMA) — Estimates that roughly 40% of small businesses never reopen after a disaster, underscoring the value of continuity planning at any size. (ready.gov / Ready Business How-To Guide)

- International Organization for Standardization (ISO 31000) — The recognized risk management standard, defining a process to identify, assess, treat, and monitor risk that applies to organizations of any size or sector. (iso.org)

Technology & Tools for Risk Management

You Don't Need an Enterprise Compliance Platform

Large companies run risk on dedicated governance, risk, and compliance (GRC) software wired into every department. A small business doesn't need to buy or run this. What you need is a way to capture your risks, decide and record how you're treating each one, and keep the proof — and you can get all three without owning enterprise software. The most common path for a small business is a shared risk register plus a compliance and recordkeeping platform provided through an HR or PEO partner, which comes pre-loaded with the required safety and harassment-prevention content and handles tracking for you.

Simple Tools That Do the Job

For everything outside formal compliance, the tools you already have are enough. A shared spreadsheet is a perfectly good risk register — one row per risk, with its scores, response, owner, and review date. A shared folder holds your policies, procedures, and insurance documents. A simple incident log captures injuries, claims, and near-misses so you can see trends. The goal isn't sophistication — it's that your risks live somewhere other than one person's worry list, and that you can see at a glance what's controlled and what isn't.

Keep Records Audit-Ready Without the Busywork

Risk management generates paperwork that matters: signed policy acknowledgments, training completions, safety inspection notes, certification and insurance renewal dates, incident reports. For a small business the danger isn't having the wrong system — it's letting these slip through the cracks until an audit or a claim makes them urgent. Date-stamped electronic records stored in one place solve most of this, and automated reminders before a certification, license, or policy lapses prevent the gap that quietly creates liability. An HR or PEO partner's platform typically handles both automatically, which is much of the value for a company without a compliance staffer to chase it.

Where AI Can Help a Small Team

AI tools have made it inexpensive for a small business to do risk work that used to need a specialist. You can use them to turn a messy brainstorm into a structured risk register, draft a first version of a safety or anti-harassment policy, summarize what a regulation actually requires, or generate a checklist tailored to your industry. That lets one busy owner or manager produce the kind of written program that used to require an outside consultant — just keep a human who knows the business and the rules reviewing anything AI produces before you rely on it, especially on compliance.

What to Prioritize

If you only fix a few things, fix these: make sure your top handful of risks each have a control and an owner, make sure the required compliance pieces are in place and documented, and make sure renewals — insurance, licenses, certifications — don't lapse. Skip the temptation to buy complex compliance software you won't fully use. A small business is better served by a one-page register, a few simple tools, and an HR partner for the compliance heavy lifting than by an enterprise platform no one has time to administer.

Key Performance Indicators (KPIs)

If you spend time and money managing risk but never check whether your exposure went down, you're guessing. The good news for a small business is that you don't need a dashboard or an analyst — you need a short list of honest signals you can glance at a few times a year. The handful below connects the work you do to the things you care about: staying compliant, avoiding losses, and keeping the business running. Track these and you'll know what's working without drowning in metrics.

A Few Metrics Worth Tracking

| What to Track | How to Read It | Target |

|---|---|---|

| Open High-Priority Risks | High or critical risks without a control and a named owner | Zero — every top risk should be assigned and being worked |

| Incidents & Near-Misses | Injuries, claims, outages, and close calls, before vs. after controls | A measurable downward trend is your proof controls work |

| Required Compliance Current | Mandated training, licenses, and certifications completed and on file | 100% — achievable with a small team |

| Insurance Coverage Gaps | Exposures with no transfer or coverage that's out of date | No material gaps; reviewed with your broker annually |

| Time to Close a Risk | How long from identifying a priority risk to having a control in place | Shorter over time means your program is maturing |

| Records Complete & Audit-Ready | Acknowledgments, training proof, and incident logs on file for everyone | 100%; this is your defense if you're ever audited or sued |

Look at these a few times a year — more often for the compliance and insurance items, less often for the rest. You don't need to model probabilities or build reports; for a small business a quick review is enough to tell you which controls to keep and which to rebuild. If pulling even these together feels like one more thing you don't have time for, it's exactly the kind of tracking an HR or PEO partner's platform handles in the background.

Frequently Asked Questions

What is the best way to manage risk in a small business?

The best way is to list what could realistically go wrong, score each risk by likelihood and impact, put controls and owners on the few that rank highest, document everything, and review the list a couple of times a year.

In a small company you don't have a risk department, so keep it simple and deliberate. Start by getting your worries onto one page — across compliance, safety, employment, financial, operational, cyber, and reputational categories. Then score each one two ways, how likely and how damaging, and use a basic likelihood-by-impact matrix to sort the long list into the handful that actually deserve money and attention.

The part most small businesses skip is follow-through, and it's the part that matters most. For each top risk, pick a response — avoid, reduce, transfer, or accept — assign one person to own it, write down what you did, and set a date to revisit it. If finding and tracking the required compliance controls is your bottleneck, that's exactly where an HR or PEO partner earns its keep.

What are the main types of business risk a small company faces?

The main types are compliance and legal, workplace safety, employment practices, financial, operational, cyber and data, and reputational — and most small businesses carry exposure in several at once.

Compliance and legal risk covers missed filings, expired licenses, and failure to meet mandated rules. Safety risk is injuries and OSHA exposure. Employment-practices risk is harassment, discrimination, and wrongful-termination claims. Financial risk is cash-flow shocks, nonpayment, and fraud, and operational risk is the everyday stuff — a key person leaving, a supplier failing, a process only one person knows.

Cyber and data risk has grown fastest, because attackers increasingly target small businesses for their thinner defenses, and reputational risk ties them all together since a single public incident can outlast the original problem. You don't have to be expert in all seven — the value of listing them is that it stops you from controlling the risk that's top of mind while ignoring a bigger one you simply hadn't thought about.

How often should a small business review its risks?

At least once or twice a year for the full list, plus a quick review immediately after any incident or major change — with compliance and insurance items checked more often.

Risk isn't static, and a register you wrote two years ago and never reopened isn't protecting you. A simple annual or twice-yearly review — re-scoring each risk, checking that controls are still in place, and adding anything new — keeps the picture honest without becoming a burden. Many small businesses tie it to a date they'll remember, like the start of the year or a renewal cycle.

Two things should trigger a review outside that schedule: an incident, because a near-miss or a claim is real-world data about where you're exposed, and a major change, like a new line of business, a key hire or departure, or a new system. Compliance and insurance items have their own clocks — licenses, certifications, and policies with fixed renewal dates — and those are the easiest things to hand to an HR partner so a lapse never sneaks up on you.

What's the difference between risk management and insurance?

Insurance is one tool within risk management — the "transfer" option — while risk management is the whole process of identifying, prioritizing, and deciding how to handle every kind of exposure.

It's a common and costly mistake to treat a stack of insurance policies as a complete risk strategy. Insurance is genuinely valuable: it shifts the financial hit of certain events — a liability claim, a workplace injury, a fire, a cyber incident — off your books and onto an insurer. But it's only one of the four ways to treat a risk, and it does nothing to prevent the event or to address risks that aren't insurable, like a key person leaving or a damaged reputation.

Risk management is the larger habit that tells you which risks to insure in the first place, which to prevent or reduce with controls, and which to simply accept. Insurance answers "who pays if it happens"; risk management answers the prior questions of "what could happen, how bad would it be, and what should we do about it." A small business needs both — and the right coverage flows naturally out of a clear-eyed look at your actual exposure.

Why does risk management matter so much for a small business?

Because in a small business a single bad event is a much larger share of the whole — one uninsured lawsuit, one serious safety citation, or one unplanned disruption can do damage a large company would absorb but a small one might not survive.

Big companies have reserves, legal teams, and diversified operations that let them absorb shocks; a small business often doesn't. The Federal Emergency Management Agency has estimated that around 40% of small businesses never reopen after a disaster, and the difference between the ones that survive and the ones that don't is usually whether they planned for disruption before it arrived. The same logic applies to a lawsuit, a breach, or the sudden loss of a key person.

Federal and state rules also require documented safety and anti-discrimination practices, and those rules don't waive themselves because you're small — if you can't show you had reasonable controls in place, you carry the risk. A small business that builds risk management into a simple routine and leans on an HR or PEO partner for the compliance and recordkeeping pieces gets much of the protection and resilience of a far larger company without needing to staff for it.

Key Takeaways

Managing risk well is within reach of any small business — it takes a clear habit, not a risk department. The same compliance obligations and the same downside apply as much to 10 employees as to 1,000, and arguably matter more when a single bad event is a far larger share of the whole.

Keep it simple and deliberate: list what could go wrong, score each risk by likelihood and impact, act on the few that rank highest, choose a response (avoid, reduce, transfer, or accept), assign an owner, document it, and revisit the list a couple of times a year and after anything major. That follow-through is what turns a list of worries into real protection.

You don't have to build the infrastructure yourself. An HR or PEO partner can supply compliance content, a platform to track and document controls, and audit-ready records — giving a small business the risk protection and resilience of a much larger one without the overhead of staffing for it.

")

")

")