What Is Workers' Compensation?

Quick Answer

Workers' compensation is a state-regulated, no-fault insurance system that pays an injured employee's medical care and part of their lost wages, no matter who was at fault. In exchange, the employer is generally shielded from being sued over that injury — a trade-off known as the exclusive remedy. Nearly every state requires it.

Workers' Compensation Defined

Workers' compensation is a mandatory insurance program, established state by state, that provides medical and wage-replacement benefits to employees who suffer a work-related injury or illness. It operates on a no-fault basis: the employee does not have to prove the employer was negligent, and the employer generally cannot argue the employee was careless. Benefits are paid because the injury happened at work — not because someone was to blame.

Key Concepts at a Glance

- No-fault benefits: An injured employee receives medical care and wage replacement without having to prove fault, which is what makes benefits fast and predictable rather than litigated.

- Exclusive remedy: In return for guaranteed benefits, the employee generally gives up the right to sue the employer over the injury. This protection is the single most valuable thing an employer buys.

- State-by-state regulation: Coverage requirements, benefit levels, filing deadlines, and medical-provider rules are set by each state, not by federal law — which is why multi-state employers face the most complexity.

- Experience-rated pricing: Premium is based on payroll, the risk class of the work being performed, and your own claims history, so safety performance directly changes what you pay.

Overview of Related Topics

- The grand bargain: Workers' comp is a century-old compromise — guaranteed benefits for workers, limited liability for employers — and nearly every rule in the system traces back to it.

- Who counts as an employee: Coverage attaches to employees, not independent contractors, which makes worker classification one of the highest-risk decisions a small business makes.

- Claims management and cost control: The premium you pay tomorrow is largely determined by how well you report, manage, and close the claims you have today.

What Workers' Comp Covers — and What It Doesn't

Workers' comp covers injuries and illnesses that arise out of and in the course of employment. That phrase does a lot of work: it is the test that decides nearly every disputed claim. Sudden accidents qualify, but so do conditions that build over time — repetitive-motion injuries, hearing loss, and occupational illnesses caused by workplace exposure.

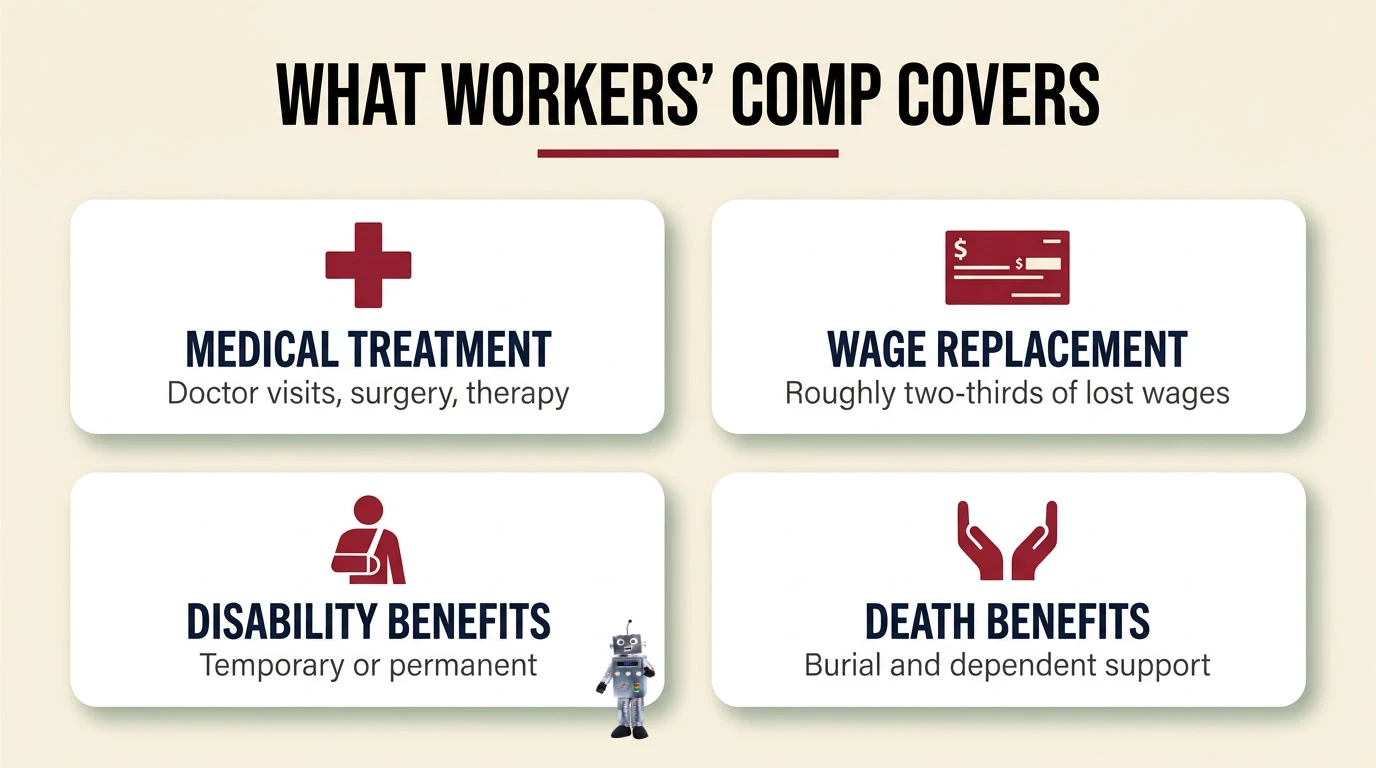

The Four Core Benefits

- Medical treatment: Doctor visits, hospital care, surgery, prescriptions, physical therapy, and medical equipment related to the injury — typically with no deductible or co-pay for the employee.

- Wage replacement (indemnity): A portion of lost wages while the employee cannot work, most commonly around two-thirds of the average weekly wage, subject to a state-set maximum and a short waiting period.

- Disability benefits: Payments scaled to whether a disability is temporary or permanent and partial or total — a sprained back that heals is treated very differently from a permanent loss of function.

- Death benefits: Burial expenses and ongoing payments to a surviving spouse and dependents when a workplace injury is fatal.

Many states add vocational rehabilitation — retraining when an employee can no longer perform their old job.

What Workers' Comp Typically Does Not Cover

This is where most employers are surprised, and where most disputes start. Coverage is generally denied when the injury falls outside the employment relationship:

- The commute: Under the "going and coming" rule, ordinary travel between home and a fixed worksite is usually not covered. Travel during the workday, or as part of the job itself, generally is.

- Intoxication and drug use: Most states allow a claim to be denied when intoxication was the cause of the injury — one reason post-accident testing policies matter.

- Horseplay and fighting: Injuries from goofing around, or from a fight the employee started, commonly fall outside coverage.

- Self-inflicted and intentional injuries: Deliberate self-harm and injuries sustained while committing a crime are excluded.

- Independent contractors: True contractors are not covered by your policy. If a worker you treat as a contractor is later reclassified as an employee, you may owe back premium, penalties, and the cost of the claim.

- Off-duty and purely personal activities: A voluntary weekend softball game is usually not covered; a mandatory company function may be.

- Ordinary illness and pre-existing conditions: Catching a cold at the office is not an occupational illness — though a work event that aggravates an existing condition often is compensable.

Two cautions. First, these exclusions are state-specific and fact-specific; the same incident can be compensable in one state and denied in another. Second, denying a claim is not the employer's call. Report it, document it, and let the carrier and the state make the determination — guessing wrong is how employers turn a small claim into a penalty.

Who Is Required to Carry Workers' Comp?

Workers' compensation is regulated at the state level, so the honest answer is: it depends on where you employ people, how many, and what work they do. The general shape of the rules is consistent even though the details are not.

The Common Patterns

- Most states require coverage from your first employee. In the large majority of states, hiring one person — full-time, part-time, or seasonal — triggers the obligation.

- A minority of states set a headcount threshold. A handful require coverage only once you reach roughly two to five employees. Because published thresholds vary and legislatures change them, verify yours with the state agency rather than a blog post.

- High-risk trades often have no threshold. Construction, roofing, trucking, and similar work commonly require coverage from the first worker — sometimes even for sole proprietors — regardless of the general state rule.

- A few states require you to buy from a state fund. In monopolistic-fund states, coverage comes from the state rather than a private carrier.

Owner, Officer, and Contractor Exemptions

Sole proprietors, partners, LLC members, and corporate officers can often exclude themselves from coverage — and often should not, since their own injuries then have no coverage at all. Two traps recur. An owner exemption removes the owner from the policy; it does not remove your obligation to cover your staff. And an uninsured subcontractor can become your responsibility: in most states, if you hire a sub without coverage and their worker is hurt, the claim lands on your policy. Collect a certificate of insurance from every sub, every time.

The Texas Exception

Texas is the only state where private employers may legally opt out of workers' compensation entirely. Employers that do are called non-subscribers, and the trade-off is severe: they give up the exclusive-remedy shield. An injured employee can sue in civil court for pain and suffering and unlimited damages, and the employer loses the common-law defenses — contributory negligence, assumption of risk, and the fellow-employee rule — that would normally limit exposure. Non-subscribers also carry their own notice and injury-reporting duties with the state.

Most Texas employers look at that math and buy coverage anyway. According to the Texas Department of Insurance, only 24% of Texas employers were non-subscribers in 2024 — the lowest share since 2016 — and just 13% of Texas employees worked for one. Opting out is legal in Texas. It is rarely the low-risk choice.

How Much Does Workers' Comp Cost?

Workers' comp is priced per $100 of payroll, not per employee. The basic formula is simple, and understanding it is the first step to controlling the bill:

(Payroll ÷ 100) × Class Code Rate × Experience Modifier = Premium

The Three Inputs

| Input | What It Is | How to Influence It |

|---|---|---|

| Payroll | Gross payroll for each class of work, the exposure base for the policy | Report it accurately by class; audits confirm estimates, and surprises at audit are almost always unpleasant |

| Class code rate | A rate per $100 of payroll assigned to each type of work; a clerical class may cost cents while a roofing class costs many dollars | Make sure employees are coded to the work they actually do — miscoding is a common and expensive error |

| Experience Modification Rate (EMR) | A multiplier based on your claims history versus expected losses for businesses like yours | The only input you control directly through safety and claims management |

The Experience Modification Rate, Explained

The experience mod is the number that turns your safety record into money. An EMR of 1.0 is average: you pay exactly what your class and payroll suggest. Below 1.0 is a credit — a 0.85 mod means you pay 15% less than an average business your size. Above 1.0 is a debit — a 1.20 mod means you pay 20% more, on every dollar of premium, every year.

Three features of the mod are worth internalizing. It is calculated on a rolling multi-year window (typically three years, excluding the most recent), so a bad year follows you. It weights claim frequency more heavily than claim severity — several small claims can hurt your mod more than one large one, because frequency predicts future losses better. And it is used for more than pricing: general contractors and public agencies frequently require an EMR below a set threshold to bid on work. A high mod doesn't just cost you money; it can cost you jobs.

What Else Moves the Price

Your industry and state are the largest levers — the same job can be priced very differently in two states. Beyond that: the number of states you operate in, your safety program and any available credits, deductible and dividend options, and whether you're in the voluntary market or the assigned-risk pool. Rates are not static, either. The National Council on Compensation Insurance (NCCI) files loss costs annually, and the recent trend has been downward — in Texas, the Department of Insurance accepted an average 3.8% decrease effective July 1, 2026. That is a tailwind, not a plan: your mod still decides where you land relative to everyone else.

Step-by-Step Guide: What to Do When an Employee Is Injured

The hours after an injury shape the entire claim. Speed is not just compassion — reporting delay is one of the strongest predictors of a claim becoming expensive and litigated. Work this sequence, in this order.

- Get medical care first. Call 911 for anything serious. For non-emergencies, direct the employee to care under your state's rules — some states let the employer or carrier designate the initial provider, others let the employee choose. Never discourage or delay treatment.

- Secure the scene and preserve evidence. Stop the work, protect anyone else at risk, and photograph the area and any equipment involved before it is cleaned up or repaired.

- Document the incident while it's fresh. Record what happened, when, where, and who saw it. Take witness statements the same day. Memory degrades fast, and thin documentation is what turns a routine claim into a contested one.

- Report the injury to your carrier immediately. File the First Report of Injury within your state's deadline — often just a few days — and don't sit on it. Fast reporting lowers claim cost, shortens duration, and reduces litigation risk. Report the claim even if you doubt it; you are not the one who decides compensability.

- Meet your state and OSHA recordkeeping duties. Log recordable injuries on your OSHA 300 log, and remember the separate OSHA reporting clocks: a work-related fatality within 8 hours, and an inpatient hospitalization, amputation, or loss of an eye within 24 hours.

- Stay in contact with the injured employee. Check in regularly and keep them connected to the workplace. Employees who feel abandoned hire attorneys; employees who feel supported come back to work.

- Bring them back on modified duty as soon as it's medically safe. Get the treating physician's restrictions in writing and offer transitional work within them. Every day of lost time adds indemnity cost — and inflates the experience mod that prices the next three years.

- Investigate the root cause and fix it. Close the loop: determine what allowed the injury, correct it, and document the correction. The claim is a cost; the same injury happening twice is a pattern, and your mod will price it that way.

Workers' Comp Compliance Checklist

Most workers' comp penalties are not the result of bad faith. They're the result of a missed posting, a late report, or a misclassified worker. Use this as a standing checklist.

Coverage and Classification

- Confirm the coverage requirement in every state where you have an employee — including remote workers, who are generally covered under the law of the state where they work.

- Verify that each employee is assigned the correct class code for the work they actually perform.

- Review every independent-contractor relationship against your state's classification test. Misclassification is the single most-penalized error in this area.

- Collect and keep a current certificate of insurance from every subcontractor.

Postings and Notices

- Display the required workers' comp notice where employees regularly gather, in the languages your state requires.

- Give new hires written notice of coverage — or, for Texas non-subscribers, written notice of no coverage.

- Keep the carrier's claim-reporting information posted and current.

Reporting and Recordkeeping

- Know your state's First Report of Injury deadline and hit it every time.

- Maintain the OSHA 300 log, 300A summary, and 301 incident reports if you're a covered employer, and post the 300A from February 1 to April 30.

- Report fatalities to OSHA within 8 hours; hospitalizations, amputations, and eye losses within 24 hours.

- Retain claim files, incident reports, and payroll records by class code — you will need them at audit.

What Non-Compliance Actually Costs

Going without required coverage is not a quiet risk. Depending on the state, employers face per-day fines that accumulate for every day uninsured, stop-work orders that shut the business down until coverage is in place, criminal exposure in some jurisdictions, and — the one that ends companies — personal liability for the full cost of an injury, with the exclusive-remedy defense stripped away. The cost of a single serious injury can exceed a decade of premium.

Reducing Claims and Premiums: Safety & Return-to-Work

Workers' comp is one of the few line items on a small business's budget that responds directly to management. You cannot negotiate your class code, and you cannot argue with your payroll. You can change your losses — and your mod turns that into money for years.

Prevention: Fewer Claims

- Target the causes that actually hurt people. Overexertion and slips, trips, and falls dominate serious injury costs across nearly every industry. Ergonomics, housekeeping, and lifting practices are not glamorous — they are where the money is.

- Train at hire, then keep training. New employees are disproportionately likely to be injured. Onboarding safety training and short, regular toolbox talks beat an annual lecture.

- Investigate near misses. A near miss is a free lesson. Treat it like a claim without a bill.

- Ask for the credits you've earned. Many states offer premium credits for drug-free workplace programs, certified safety programs, or written safety plans. Ask your carrier what's available in your state.

Return-to-Work: Shorter, Cheaper Claims

A formal return-to-work (RTW) program is the highest-leverage cost control most small employers don't have. The logic is straightforward: indemnity payments accrue while an employee sits at home, and a claim that stays open drifts toward litigation. Bring the employee back on transitional or modified duty within the physician's written restrictions and you cut indemnity cost, shorten claim duration, and protect the mod.

Build it before you need it. Write the policy, pre-identify a menu of light-duty tasks that are real work, and train supervisors on how to respond to an injury without improvising. When the call comes, you follow the plan instead of inventing one.

Claims Management: Lower Cost Per Claim

Report immediately. Stay in contact with the injured employee and the adjuster. Review open claims and reserves with your carrier — an open claim with an inflated reserve is still hurting your mod, so push to get claims accurately reserved and properly closed. And audit your loss runs and mod worksheet for errors; they are more common than employers assume, and a corrected mod pays you back on every premium dollar.

Key Performance Indicators (KPIs)

Workers' comp is one of the few areas of HR with genuinely standardized metrics — and one of them, the experience mod, is literally priced into your premium. Track these, benchmark them against your industry, and you will see cost problems long before the renewal quote does.

| KPI | What It Measures | Why It Matters |

|---|---|---|

| Experience Modification Rate (EMR) | Your claims history versus expected losses for your class and size; 1.0 is average | Multiplies your premium directly and often gates your ability to bid on contract work |

| TRIR (Total Recordable Incident Rate) | Recordable injuries per 100 full-time workers per year | The standard safety benchmark; the 2024 private-industry average was 2.3 per 100 FTE |

| DART Rate | Cases involving days away, restricted duty, or job transfer, per 100 workers | Isolates the injuries serious enough to cost real money; the 2024 private-industry average was 1.4 |

| Lost-Time Claim Rate | Share of claims that move beyond medical-only into wage replacement | Lost-time claims cost dramatically more than medical-only; this is the ratio to attack |

| Claim Lag Time | Days between the injury and the report to the carrier | The most controllable predictor of claim cost — every day of delay raises severity and litigation risk |

| Average Cost Per Claim | Total incurred cost divided by number of claims | Reveals whether your problem is frequency (many small claims) or severity (a few big ones) |

| Return-to-Work Rate | Share of injured employees back on the job — including modified duty — within a target window | The clearest indicator that your RTW program is real rather than written down |

| Claim Closure Ratio | Claims closed versus claims opened over a period | Open claims with stale reserves keep inflating your mod long after the employee has recovered |

If you track only two, track claim lag time and EMR: one is the input you control today, and the other is the price you'll pay for it tomorrow.

Workers' Comp Statistics & Outlook

The data tells a genuinely surprising story: workplace injuries keep getting rarer, and individual claims keep getting more expensive. Figures below come from the U.S. Bureau of Labor Statistics, the National Council on Compensation Insurance, and the National Safety Council.

Injuries Are Falling

- Private employers reported about 2.5 million nonfatal workplace injuries and illnesses in 2024, down 3.1% from 2023.

- The total recordable case rate fell to 2.3 per 100 full-time workers — the lowest in the series going back to 2003.

- NCCI reported that lost-time claim frequency declined 2% in 2025, continuing a long-running trend.

- There were 5,070 fatal work injuries in 2024, down 4.0% from the prior year.

But Claims Are Getting More Expensive

- NCCI reported that both medical and indemnity severity rose 4% in 2025 — injured workers are receiving more, and more complex, care.

- The average workers' comp claim for accidents in 2022–2023 was $47,316. Costs by cause run far higher: falls and slips near $54,500, and motor-vehicle claims above $91,000.

- The National Safety Council put the total cost of U.S. work injuries at roughly $181 billion in 2024, or about $48,000 per medically consulted injury in economic cost to society.

The Market Outlook

Workers' comp remains one of the strongest-performing major lines in property and casualty insurance — NCCI reported a 91% calendar-year combined ratio for 2025 and its twelfth consecutive year of underwriting profitability, with net written premium essentially flat at $41.6 billion. That profitability has pushed loss costs down across nearly every state, and approved NCCI filings are expected to reduce written premium by an average of about 5% from 2025 to 2026.

What this means for a small business: the market is a mild tailwind right now, but the underlying trend — fewer claims, each one costing more — means a single serious injury carries more weight than it used to. Prevention and fast, disciplined claims handling matter more in a low-frequency, high-severity world, not less.

Workers' Comp and PEOs

Workers' comp is the piece of employer risk that small businesses are least equipped to carry alone. It requires insurance placement, multi-state compliance, claims management, safety programming, and someone who can read a mod worksheet. This is one of the main reasons businesses turn to a professional employer organization (PEO).

How the Arrangement Changes Things

- Access through pooling: Under co-employment, the PEO arranges coverage for its worksite employees as a group. That pooled buying power can open the market to businesses that would otherwise land in the assigned-risk pool — and it can stabilize pricing for high-risk class codes.

- Professional claims management: Claims are reported, tracked, reserved, and closed by people who do it every day. Given that reporting speed and claim closure are the two biggest levers on cost, this is where much of the value sits.

- Safety and loss control included: Most PEOs provide safety programming, site assessments, and OSHA-recordkeeping support — services a 30-person company rarely staffs internally.

- Multi-state compliance handled: Coverage requirements, postings, and reporting deadlines vary by state. A PEO manages that patchwork as a matter of course.

- Administrative simplification: Premium is typically billed with payroll rather than through a large down payment and year-end audit, which smooths cash flow — a real benefit for seasonal and growing businesses.

What to Ask Before You Sign

Not all arrangements are alike. Ask how workers' comp is priced and billed, how claims are handled and by whom, what happens to your loss history and experience mod if you leave, and what safety services are actually included versus sold separately. As with any PEO relationship, get it in the Client Service Agreement rather than on a slide.

Other Common Workers' Comp Questions

Is Workers' Comp the Same as Disability Insurance?

No. Workers' comp covers injuries and illnesses caused by the job. Short- and long-term disability insurance covers conditions that are not work-related. They are separate systems with separate funding, and one does not substitute for the other.

Does Workers' Comp Cover Remote Employees?

Yes. An employee injured while performing work duties at home is generally covered, and coverage typically follows the law of the state where they work — which is why a single remote hire in a new state can create a new compliance obligation. The hard part isn't coverage; it's proving the injury arose out of the work rather than the household. Clear expectations about work hours and workspace help.

Can an Employee Be Fired While on Workers' Comp?

Being on a claim doesn't make an employee untouchable, but retaliation for filing a claim is illegal in every state, and the appearance of retaliation is where employers get into trouble. Any employment action involving an employee with an open claim deserves careful documentation and, usually, professional guidance before you act.

What Is Employer's Liability Coverage?

Standard workers' comp policies include a second part — employer's liability — that responds to injury lawsuits falling outside the exclusive-remedy shield. It's the backstop for the edge cases, and it's part of why "just paying the medical bill" is not a substitute for a policy.

Frequently Asked Questions

What is workers' compensation in simple terms?

Workers' compensation is a no-fault insurance system that pays an employee's medical bills and part of their lost wages when they're hurt on the job — no matter who was at fault — and in exchange generally protects the employer from being sued over that injury.

Every state runs its own system, so benefit levels, deadlines, and coverage rules vary. The trade-off at the heart of it is the same everywhere: guaranteed benefits for the worker, limited liability for the employer.

Is workers' comp required in Texas?

No. Texas is the only state where private employers can legally opt out of workers' compensation. Employers that opt out are called non-subscribers — and they lose the exclusive-remedy protection that limits injury lawsuits.

A non-subscriber can be sued directly by an injured employee for unlimited damages, without the usual defenses of contributory negligence, assumption of risk, or the fellow-employee rule. In 2024, 76% of Texas employers carried coverage anyway — the highest share since 2016 — covering 87% of the state's employees.

How much does workers' comp cost?

Premium is calculated per $100 of payroll: (payroll ÷ 100) × your class code rate × your experience modifier. Cost therefore depends far more on the type of work and your claims history than on your headcount.

A clerical class code may cost cents per $100 of payroll while a roofing class costs many dollars. Your experience mod then multiplies the whole thing — a 1.20 mod costs you 20% more every year, and a 0.85 mod saves you 15%, which is why safety and claims management are the real cost controls.

Does workers' comp cover independent contractors?

Generally no — workers' comp covers employees, not true independent contractors. But misclassification is one of the most heavily penalized mistakes an employer can make.

If a worker you treat as a contractor is later determined to be an employee, you may owe back premium, penalties, and the full cost of the injury. In most states, hiring an uninsured subcontractor can also push their worker's claim onto your policy — so collect a certificate of insurance from every sub.

Can an employee sue me if I have workers' comp coverage?

In most cases, no. That's the exclusive-remedy rule: in exchange for guaranteed no-fault benefits, employees generally give up the right to sue their employer over a workplace injury.

The exceptions are narrow — typically intentional harm or, in some states, gross negligence — and employer's liability coverage in the policy exists to respond to them. The protection disappears entirely, however, if you were required to carry coverage and didn't, or if you're a Texas non-subscriber.

What happens if I don't carry required workers' comp?

Penalties vary by state but commonly include per-day fines, stop-work orders that halt operations, criminal exposure in some states, and personal liability for the entire cost of an injured employee's claim.

The costly part isn't the fine — it's losing the exclusive-remedy shield. With the average claim near $47,000 and serious injuries running well into six figures, the cost of a single accident can exceed years of premium.

Key Takeaways

Workers' compensation is a no-fault system that pays medical costs and lost wages for job-related injuries and, in return, generally shields the employer from being sued. It covers medical care, wage replacement, disability, and death benefits — and it generally does not cover the ordinary commute, intoxication, horseplay, self-inflicted injuries, or independent contractors. Nearly every state requires it; Texas alone lets private employers opt out, and doing so trades a premium for unlimited lawsuit exposure.

Cost is driven by payroll, class code, and your experience modifier — and the mod is the one input you control. Reporting claims fast, bringing employees back on modified duty, and fixing the causes of injury are what move it. Claim lag time and EMR are the two numbers worth watching: one is what you do today, the other is what you'll pay for your next three years.

The broader trend makes discipline more valuable, not less: injuries are at their lowest recorded frequency while the cost of each claim keeps climbing. For small businesses without an internal safety and claims function, a PEO is often the most practical way to get pooled coverage, professional claims management, and safety support — and to make sure one bad afternoon never becomes the thing that ends the business.

This article was drafted with the assistance of AI and edited and reviewed by David Cartmel. It is general HR guidance, not legal, tax, or financial advice. Workers' compensation requirements vary by state and change over time — confirm your obligations with your state agency or a licensed professional.

")

")

")