Challenges of Running a Small Business

Quick Answer

Running a small business means doing the work of an entire company with a fraction of its resources. The most common challenges cluster into a handful of areas: cash flow and thin margins, finding and keeping good people, carrying the full weight of HR, payroll, and compliance with no dedicated department, offering benefits that compete with larger employers, and finding enough hours in the day while wearing every hat at once. Layer on marketing and customer acquisition and the strain of managing growth, and it becomes clear why roughly one in five new businesses does not survive its first year. The encouraging part: most of these are systems-and-support problems, not fatal flaws. With the right processes, tools, and partners — a bookkeeper or fractional CFO for the money side, and a PEO (professional employer organization) for the people side — a small business can shoulder big-company complexity without a big-company headcount.

The Biggest Challenges of Running a Small Business

Almost every small-business challenge traces back to the same root: a small team is being asked to do everything a large company does, without the departments, specialists, or cash cushion of a large company. The specific hurdles show up in predictable places. Here are the ones owners run into most. This is general guidance, not legal, tax, or financial advice — your situation may weight these differently.

The Core Challenges

- Cash flow and thin margins: Money owed but not yet collected, uneven revenue, and a small buffer mean a single late-paying customer or surprise expense can turn a slow month into a crisis. Cash flow is the mechanism through which most other problems become fatal.

- Hiring and retaining good people: Small employers compete for talent against companies with recruiters, name recognition, and richer pay and benefits — and every departure hits harder when the team is small.

- The HR, payroll, and compliance burden: Payroll taxes, wage-and-hour rules, ACA reporting, new-hire paperwork, and multi-state registrations all still apply with a headcount of five, but there is usually no one whose job it is to handle them.

- Offering competitive benefits: On its own, a small group has little leverage with insurance carriers, so health, dental, vision, and retirement plans are often expensive and thin — exactly the thing candidates compare when choosing an employer.

- Time and wearing too many hats: The owner is often the salesperson, bookkeeper, HR manager, and janitor. Every hour on administrative upkeep is an hour not spent on customers, product, or growth.

- Marketing and customer acquisition: A great product still has to be found and bought. Without a clear market, message, and channel, even good businesses stall.

- Managing growth and scaling: Growth is the goal, but it strains everything — cash, systems, hiring, and the owner's attention. Scaling too fast without a foundation breaks businesses as surely as never growing at all.

- Rising costs and economic pressure: Inflation, rising insurance premiums, and higher borrowing costs squeeze already-thin margins and make every other challenge harder to absorb.

Which Ones Actually Sink Businesses

Not every challenge is equally dangerous. When researchers look at why businesses close, two causes dominate: building something the market does not need, and simply running out of cash. Nearly everything else — weak marketing, bad hires, compliance penalties, owner burnout — tends to work by draining cash or eroding demand until one of those two becomes terminal. That is good news for planning: fix the money and the market first, then systematically remove the drains on both.

Why Running a Small Business Is So Hard

It helps to name why these challenges hit small businesses harder than large ones. It is rarely a matter of the owner working less hard — usually the opposite. The difficulty is structural, and understanding the structure is the first step to working around it.

No Dedicated Departments

A large company has an accounting team, an HR team, a benefits broker, an IT department, and a legal function. A small business has the owner, maybe a part-time bookkeeper, and a stack of deadlines nobody has time to track. The same work still exists; it just lands on people who were hired to do something else.

Thin Margins and Little Cushion

Small businesses tend to run with a narrow buffer — often only a few weeks of operating cash on hand. That leaves almost no room for a mistake, a slow season, or a customer who pays late. Big companies absorb those shocks; small ones feel every one of them.

Competing Against Bigger Employers for Talent

When a small business and a large one chase the same candidate, the large one usually offers better benefits, more predictable hours, and a recognizable name. Without a way to close that gap, small employers lose good people to companies that can simply out-package them.

Complexity That Grows With You

Employment law, tax obligations, and compliance requirements multiply as you add employees, locations, and states. A business that felt simple at three people can feel legally and administratively heavy at fifteen — and the penalties for getting it wrong do not scale down for small size.

The Owner as a Single Point of Failure

In most small businesses, the owner is the one person who understands the whole operation. That concentration makes the business fragile: when the owner is sick, stretched, or simply out of hours, everything slows. Much of the art of running a small business is reducing how much depends on any one person — starting with the owner.

The People Side: HR, Payroll, Benefits & Compliance Challenges

Of all the challenges above, the "people side" is both the heaviest and the most overlooked, because it is invisible until something breaks. It is also the cluster where the most costly mistakes hide. Here is what it actually contains.

Payroll and Employment Taxes

Payroll looks simple until you factor in withholding, filing and remitting federal, state, and local employment taxes, issuing W-2s, handling garnishments, and new-hire reporting — on a strict schedule, with penalties for errors. A single missed deposit or misclassified worker can trigger fines that dwarf the time saved by doing it in-house.

Benefits That Attract Talent

Health, dental, vision, and retirement plans are often the deciding factor when a candidate chooses between employers. But small groups face steep rates and limited options on their own, which leaves many small businesses either overpaying or offering less than they would like — and losing recruits because of it.

HR Compliance and Employment Law

Wage-and-hour rules, ACA reporting, COBRA, anti-discrimination law, required postings, handbooks, documentation, and termination procedures make up a dense landscape where honest mistakes are common and expensive. Most small businesses have no specialist watching this, so gaps go unnoticed until a claim or audit surfaces them.

Workers' Compensation and Workplace Safety

Coverage requirements, claims management, and safety programs are their own specialty. Handled poorly, they raise premiums and expose the business to liability; handled well, they protect both employees and the bottom line.

The Hidden Time Cost

Even when nothing goes wrong, the people side quietly eats hours — reconciling payroll, chasing a benefits question, filing a form, answering an employee's request. That time comes directly out of the work only the owner can do. This is precisely the cluster a PEO is built to absorb, which is where the next sections lead.

The Real Cost of Getting These Wrong

Challenges left unmanaged do not stay abstract — they show up as money, time, and stress. Making the stakes concrete is often what turns "I'll get to it" into action.

Where the Costs Land

- Compliance penalties: Payroll-tax errors, missed ACA filings, wage-and-hour violations, and misclassification can each carry fines, back pay, and interest — costs that arrive all at once and often at the worst time.

- Turnover: Replacing an employee is expensive once you count recruiting, onboarding, lost productivity, and the strain on the coworkers who cover the gap. On a small team, one departure can stall an entire function.

- Cash-flow shocks: A late receivable or surprise bill, against a thin buffer, can force an owner to skip their own pay, delay payroll, or take on costly short-term debt.

- Owner burnout: The least-measured cost and one of the most dangerous. When the person the business depends on runs out of energy, judgment and growth both suffer.

- Failure itself: The ultimate cost. Most closures are the end point of smaller problems — weak demand and drained cash — that were survivable earlier and became fatal only after compounding.

The pattern worth remembering: these costs are rarely a single catastrophe. They accumulate quietly and then surface together. Addressing the challenges while they are still small and cheap is almost always less expensive than absorbing the consequences later.

Statistics & Outlook

The numbers put the challenges in perspective — both how common failure is and how much the right support changes the odds. These figures come from the U.S. Bureau of Labor Statistics, the U.S. Small Business Administration, and NAPEO (the PEO industry association). They are updated periodically, so treat them as a snapshot and check the sources for the latest.

What the Data Shows

- Survival is hard, but not a coin flip. BLS data shows roughly one in five new businesses (about 20%) close in their first year, close to half by year five, and about two-thirds by year ten. The first year is the steepest; odds improve markedly for those who get past it.

- Cash flow is the common thread. Cash-flow problems are implicated in the large majority of small-business failures. Research on business banking has found the typical small business holds only about a month of cash buffer — meaning a few weeks without inflows can be existential.

- Demand matters most. Studies of failed companies repeatedly find "no market need" among the top causes, cited in roughly a third or more of cases — a reminder that marketing and product-market fit are survival issues, not luxuries.

- Benefits keep getting pricier. Health-insurance premiums have risen sharply in recent years, widening the gap between what large and small employers can offer and making pooled buying power more valuable to small teams.

The PEO Difference

For the people-side cluster specifically, NAPEO-commissioned research on businesses that use a PEO found they:

- Grow more than twice as fast as comparable businesses that do not use one.

- Have employee turnover roughly 12% lower.

- Are about 50% less likely to go out of business in a given year.

- See a positive average return on investment in cost savings alone, with the survival advantage strongest for the very smallest businesses.

The Outlook

The broad trend is toward more outsourcing of HR, not less. As employment regulation grows more complex and small businesses compete for talent against larger employers, the case for pooled benefits, professional compliance, and reclaimed owner time keeps strengthening. The practical takeaway is that most of the hardest challenges are now well-understood problems with well-established solutions — the work is choosing and applying them before the costs compound.

How to Overcome Small Business Challenges: A Step-by-Step Approach

You cannot fix everything at once, and you do not need to. The most resilient small businesses tackle challenges in an order that protects cash and demand first, then removes the drains on both. Here is a sequence that works.

- Get a clear, current picture of your cash: Know your true margins, your runway in weeks, and which customers pay slowly. You cannot manage cash flow you cannot see, and almost every other decision depends on this one.

- Confirm the market actually wants what you sell: Talk to customers, watch what they buy versus what they say, and sharpen your message and pricing. Fixing demand is more powerful than any cost cut.

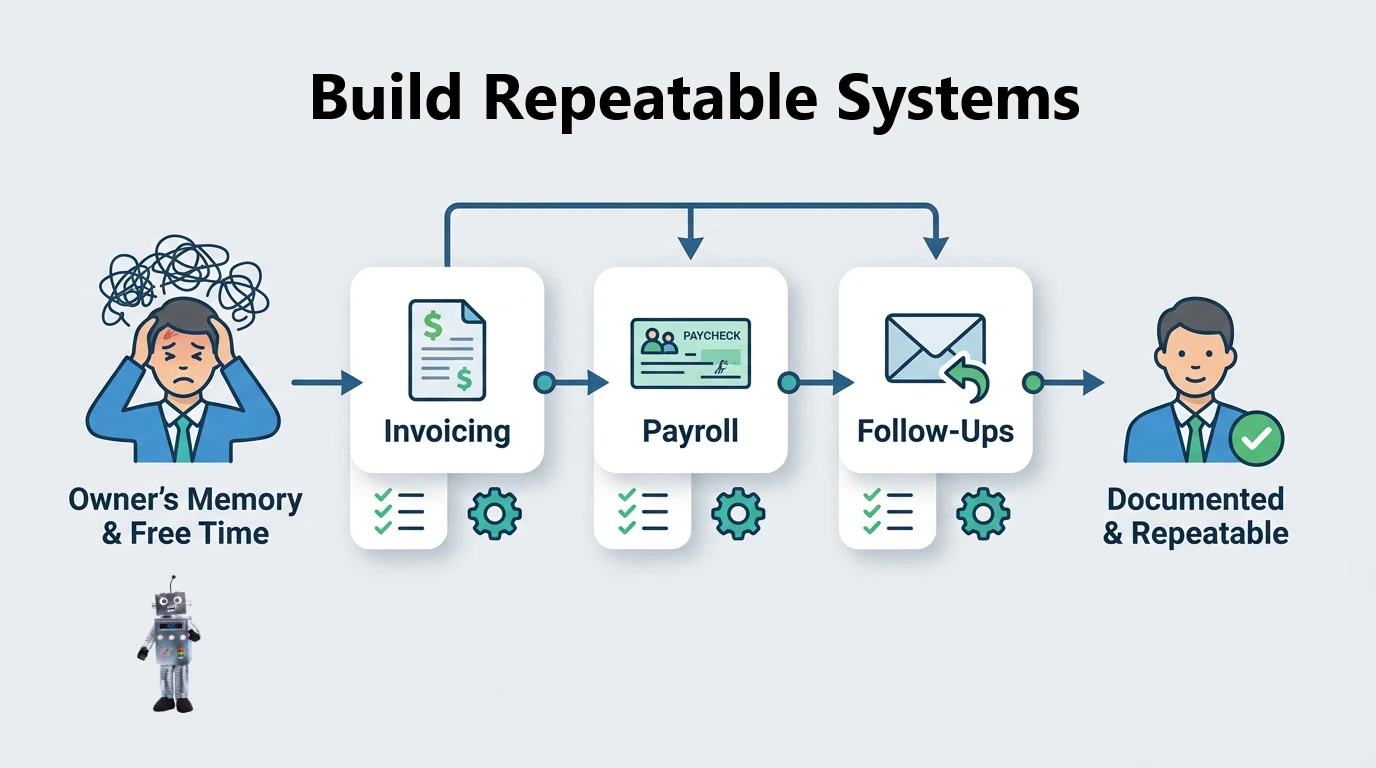

- Build repeatable systems for the back office: Turn recurring tasks — invoicing, payroll, follow-ups — into documented, repeatable processes so they stop depending on the owner's memory and free time.

- Get your HR, payroll, and compliance house in order: Make sure payroll taxes, filings, classifications, and required documentation are correct and current. This is where small, invisible gaps become large, expensive ones.

- Make your benefits competitive: Look for ways to offer health, retirement, and other benefits at rates a small group cannot usually reach alone — often through pooling with a larger group — so you can recruit and keep good people.

- Protect your time — delegate or outsource what isn't your core work: Identify the tasks that do not require the owner and hand them to a person, a tool, or a partner. Reclaimed hours are the highest-return investment a small business can make.

- Plan for growth before it arrives: Decide in advance how you will handle more customers, more employees, and more locations, so scaling strengthens the business instead of breaking it.

Challenge-and-Solution Table

Here is each major challenge alongside a practical fix you can start on yourself, and how a PEO addresses the people-side pieces specifically. Not every challenge is a PEO's job — cash flow and marketing are yours to lead — but the HR cluster is exactly what a PEO is built for.

| Challenge | Practical Fix | How a PEO Helps |

|---|---|---|

| Cash flow & thin margins | Track runway weekly; tighten receivables; keep a reserve | Indirectly — predictable HR costs and fewer penalty surprises stabilize outflows |

| Hiring & retention | Sharpen your offer and onboarding; move faster than big competitors | Big-company benefits and professional HR make you more attractive and lower turnover |

| Payroll & employment taxes | Use reliable payroll software or a specialist | Processes payroll, withholds and remits taxes, issues W-2s, handles filings |

| Competitive benefits | Shop plans; consider pooling for better rates | Pools your team with others to unlock richer plans at better rates |

| HR compliance & employment law | Keep documentation current; get expert review | Provides compliance support across ACA, wage-and-hour, and more |

| Workers' comp & safety | Maintain coverage and a safety program | Arranges coverage and helps manage claims and risk |

| Time & wearing too many hats | Delegate and outsource non-core work | Absorbs the HR back office, returning hours to the owner |

| Marketing & customer acquisition | Clarify your market, message, and channels | Not a PEO function — but reclaimed time lets you focus here |

| Managing growth & multi-state | Plan systems and hiring ahead of demand | Supports multi-state compliance and scales HR as you add people |

How a PEO Helps Small Businesses Meet These Challenges

A PEO (professional employer organization) exists to solve the people-side cluster that quietly drains small businesses. Through a co-employment arrangement, the PEO becomes the administrative employer for your team — handling payroll, benefits, workers' comp, and compliance — while you keep full day-to-day control of your people and your business. Here is where that shows up against the challenges above.

Enterprise-Grade Benefits at Small-Business Scale

By pooling your employees with those of other clients, a PEO can offer health, dental, vision, and retirement plans priced like a large employer's — a direct answer to the recruiting-and-retention gap that costs small businesses good people.

Compliance and Risk, Handled by Specialists

Payroll taxes, ACA reporting, workers' comp, and employment-law questions move from the owner's overloaded plate to dedicated specialists, lowering the odds of the costly mistakes that surface in audits and claims.

Hours Back to Run the Business

Offloading the HR back office returns time to the owner and managers — time that goes to customers, cash flow, and growth, the work only they can do.

You Keep Control

This is the most common worry, and the answer is reassuring: your employees still report to you, are hired and let go by you, and take direction from you. The PEO handles the paperwork of being an employer, not the running of your business. It is a real legal and financial relationship governed by a service agreement, so it is worth comparing providers and having an attorney review the contract.

Small Business Challenge Self-Assessment Checklist

Use this to find where your business is most exposed. The items you cannot confidently check are your priorities. This is a self-assessment.

Cash & Financial Health

- You know your true profit margins and your runway in weeks, not just your bank balance.

- You have a cash reserve that could cover a slow month or a surprise expense.

- You track which customers pay late and act on it.

People & HR

- Payroll and employment taxes are processed accurately and on schedule.

- Your benefits are strong enough to compete for the people you want to hire.

- Turnover is low, and losing one person would not stall an entire function.

Compliance & Risk

- You are confident you are current on wage-and-hour rules, ACA, and required documentation.

- You are properly registered and covered in every state where you have employees.

- Workers' comp coverage and a basic safety program are in place.

Time & Focus

- The owner spends most of their time on core work, not administrative upkeep.

- Recurring tasks run as documented systems, not from memory.

- You have a plan for how growth will be handled before it arrives.

Topics

The Biggest Challenge in the First Year

The first year is the riskiest, and the biggest challenge is usually staying solvent long enough to find product-market fit. That means confirming real demand, keeping the burn rate low, and protecting cash while you learn what customers will actually pay for. Almost every other first-year problem is survivable if cash and demand hold.

The Challenges of Scaling a Growing Business

Growth introduces a different set of problems than survival. Systems that worked at five employees strain at fifteen; the owner becomes a bottleneck; and hiring, payroll, and compliance complexity all climb at once. Scaling well is largely about building processes and support — and delegating the back office — before the growth forces the issue.

Multi-State and Remote-Team Challenges

The moment you employ people in more than one state, compliance multiplies: separate registrations, tax accounts, and varying labor laws. For small businesses with remote or distributed teams, this is one of the fastest-growing and most underestimated challenges — and one of the more common reasons owners turn to a partner that already operates across states.

Frequently Asked Questions

What are the biggest challenges of running a small business?

The most common challenges are managing cash flow and thin margins, hiring and retaining good people, carrying the HR, payroll, and compliance burden without a dedicated department, offering competitive benefits, protecting the owner's time, marketing and customer acquisition, and managing growth.

Most of these come from the same root: a small team doing everything a large company does without the departments, specialists, or cash cushion. That framing is also why the right systems, tools, and partners make such a difference.

Why do most small businesses fail?

Two causes dominate: building something the market does not need, and running out of cash. Most other problems — weak marketing, bad hires, compliance penalties, burnout — work by draining cash or eroding demand until one of those becomes terminal.

BLS data shows roughly one in five new businesses closes in the first year and about half within five years, with cash-flow problems implicated in the large majority of closures. Fixing demand and protecting cash first addresses the biggest risks.

What is the hardest part of running a small business?

For most owners it is the combination of too little time and too many roles. When one person is the salesperson, bookkeeper, HR manager, and problem-solver, the back office quietly consumes the hours that should go to customers and growth.

That is why reclaiming the owner's time — by delegating, systematizing, or outsourcing non-core work such as HR and payroll — is often the highest-return move a small business can make.

How can a small business compete with larger employers for talent?

The gap is usually benefits and stability, not the work itself. Small businesses close it by offering competitive health and retirement benefits — often through pooling with a larger group to reach better rates — and by moving faster and more personally than big employers can.

Pooled benefits and professional HR support are a large part of why businesses that use a PEO tend to have lower turnover than comparable companies.

Can a PEO help with the challenges of running a small business?

Yes, for the people-side cluster specifically. A PEO handles payroll, benefits, workers' comp, and HR compliance through a co-employment arrangement, while you keep full day-to-day control of your team and your business.

Research on businesses that use a PEO finds they tend to grow faster, have lower turnover, and are significantly less likely to go out of business. A PEO will not fix cash flow or marketing for you, but it removes much of the HR weight so you can focus there.

Key Takeaways

Running a small business is hard for structural reasons: a small team is asked to do everything a large company does, without the departments, specialists, or cash cushion. The challenges cluster into a predictable set — cash flow and thin margins, hiring and retention, the HR and compliance burden, competitive benefits, the owner's time, marketing, and growth — and two of them, weak demand and drained cash, are what actually sink most businesses.

The costs of leaving these unmanaged are concrete: compliance penalties, turnover, cash-flow shocks, owner burnout, and, ultimately, failure. They rarely arrive as one catastrophe; they accumulate quietly and surface together, which is why addressing them while they are small is far cheaper than absorbing the consequences later.

The encouraging part is that most of these are well-understood problems with well-established solutions. Protect cash and confirm demand first, then systematically remove the drains on both — including by handing the people side to a partner built for it. Businesses that outsource HR to a PEO tend to grow faster, keep employees longer, and survive at higher rates, because the owner gets big-company capability and their own time back without a big-company headcount.

")

")