Group Health Insurance

What Is Group Health Insurance?

Group Health Insurance is an employer-sponsored health coverage plan that insures a defined group of individuals—typically employees and their eligible dependents—under a single policy. It encompasses medical, dental, vision, and prescription benefits, with premiums shared between employer and employee. For organizations, it is a core compensation component that drives talent acquisition, reduces absenteeism, and fulfills workforce duty-of-care obligations.

Core Coverage Components

- Medical Benefits: Covers inpatient and outpatient care, preventive services, emergency treatment, and specialist visits, typically subject to deductibles, copays, and out-of-pocket maximums.

- Dental and Vision Coverage: Often offered as supplemental elections within the group plan, covering routine exams, cleanings, corrective lenses, and basic restorative procedures.

- Prescription Drug Coverage: Structured around tiered formularies that determine cost-sharing levels based on whether drugs are generic, preferred brand, or specialty.

Overview of Related Topics

- Plan Structures and Delivery Models: Group health plans are offered primarily as HMO, PPO, EPO, or HDHP models, each differing in network flexibility, referral requirements, and employee cost-sharing levels. HDHPs are frequently paired with Health Savings Accounts (HSAs) to offset out-of-pocket exposure.

- Key Stakeholders and Roles: Employers act as plan sponsors, insurers or TPAs administer benefits, and brokers advise on plan design and carrier selection. Employees are participants who elect coverage during open enrollment or qualifying life events.

- Regulatory and Compliance Framework: Group health plans are governed primarily by ERISA, ACA, HIPAA, and COBRA. ACA employer mandates require organizations with 50 or more full-time equivalent employees to offer minimum essential coverage or face tax penalties.

- Cost Structure and Employer Considerations: Premium costs are split between employer and employee, with employers typically covering 70–80% for individual coverage. Plan design decisions directly affect total compensation benchmarking, workforce attraction, and annual benefits budget.

Plan Structures, Stakeholders & Compliance

Plan Structures and Delivery Models

- HMO (Health Maintenance Organization): Requires members to select a primary care physician and obtain referrals for specialist care; limited to in-network providers, resulting in lower premiums.

- PPO (Preferred Provider Organization): Allows employees to see any provider without a referral, with lower cost-sharing for in-network visits; offers maximum flexibility at a higher premium cost.

- HDHP with HSA: High-deductible health plans paired with employer- or employee-funded HSAs shift more initial cost to employees while enabling pre-tax savings for qualified medical expenses.

Key Stakeholders and Roles

- Plan Sponsor (Employer): Legally responsible for plan design, funding, vendor selection, and ACA compliance; files Form 5500 annually for self-funded plans subject to ERISA reporting.

- Third-Party Administrator (TPA) or Insurer: Processes claims, manages provider networks, and administers utilization management for either fully insured or self-funded arrangements.

- Benefits Broker or Consultant: Advises HR and finance teams on carrier negotiations, benchmarking, renewal strategy, and regulatory updates; compensated via carrier commissions or flat consulting fees.

Regulatory and Compliance Framework

- ACA Employer Shared Responsibility: Applicable Large Employers (ALEs) with 50+ FTEs must offer minimum essential, minimum value coverage to full-time employees or face IRS penalties under Sections 4980H(a) and (b).

- COBRA Continuation Coverage: Requires employers with 20 or more employees to offer terminated or otherwise ineligible participants the option to continue group coverage for up to 18–36 months at full premium cost.

- HIPAA Portability and Privacy: Prohibits coverage exclusions based on pre-existing conditions, mandates special enrollment rights, and governs the confidentiality of protected health information (PHI) held by plan administrators.

Cost Structure and Employer Considerations

- Premium Contribution Strategy: Employer contribution rates—typically 70–80% for employee-only coverage and 50–65% for dependent tiers—are benchmarked against industry surveys such as KFF or Mercer to remain competitive.

- Fully Insured vs. Self-Funded: Fully insured plans transfer risk to the carrier in exchange for fixed premiums; self-funded plans retain claims risk but offer greater design flexibility and exemption from state insurance mandates.

- Total Cost of Benefits: Group health premiums represent the largest single line item in most benefits budgets, requiring annual actuarial review, utilization analysis, and plan design adjustments to manage trend.

A Closer Look

Group health insurance is one of the most consequential benefits an organization can offer its workforce. As an employer-sponsored health coverage plan, it provides employees and their eligible dependents with access to medical, dental, vision, and prescription drug benefits under a single group policy. Premiums are shared between employer and employee, making coverage more affordable than individual market alternatives. Organizations offer group health insurance because it directly supports workforce health, reduces absenteeism, and fulfills a fundamental duty of care to employees. It is not a peripheral benefit — it is a central pillar of a competitive total compensation strategy.

HR professionals and benefits teams are the primary architects of group health insurance programs, working alongside brokers, carriers, and third-party administrators to design, communicate, and manage an employee benefits plan that meets both organizational budget constraints and employee needs. Employees at every level rely on this coverage — from hourly workers managing chronic conditions to executives coordinating family care. When group medical insurance is structured well, it reduces turnover, strengthens recruitment outcomes, and demonstrates that an organization invests in the people who drive its performance. Benefits professionals who manage this function hold significant influence over employee wellbeing and organizational culture.

Key Infographic Statistics at a Glance

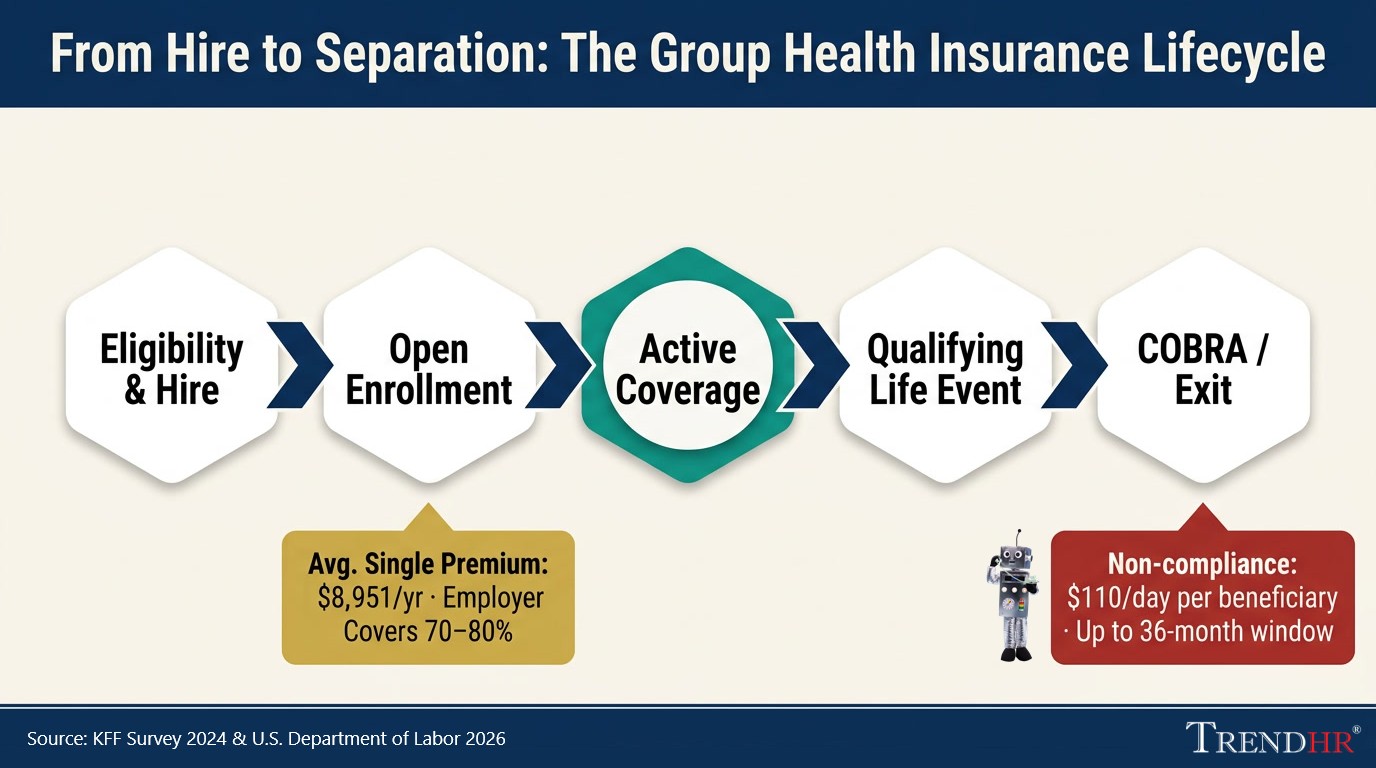

- $8,951 — average annual premium for single coverage (KFF Employer Health Benefits Survey, 2024), rising to $25,572 for family coverage

- 70–80% — typical employer share of the single-coverage premium, with employees covering the remainder through pre-tax payroll deductions under IRS Section 125 cafeteria plan rules

- 18–36 months — COBRA continuation window available to terminated employees and qualifying dependents, at full premium cost plus up to a 2% administrative fee

- $110/day — statutory penalty per qualified beneficiary for COBRA notice non-compliance under (ERISA / DOL), making timely notice issuance a hard compliance deadline

- 50+ FTEs — the ACA Applicable Large Employer threshold triggering mandatory minimum essential coverage obligations under (IRC § 4980H), with penalties assessed per full-time employee for non-compliant plans

Statistics & Outlook

Group health insurance is an employer-sponsored health coverage arrangement in which a single policy covers a defined group — typically employees and their eligible dependents — with premiums shared between employer and plan participants. Under the Affordable Care Act, employers with 50 or more full-time equivalent employees must offer minimum essential, minimum value coverage to their full-time workforce or face tax penalties under IRC Sections 4980H(a) and (b). The IRS further requires employers to report the aggregate cost of this coverage on employees' Form W-2, though the employer's premium contribution remains excludable from taxable income — a structural tax advantage that makes group coverage substantially more cost-efficient than individual market alternatives for both parties (IRS).

Access to group health insurance varies significantly across the wage spectrum. According to the U.S. Bureau of Labor Statistics, only 26% of private industry workers in the lowest 10% wage bracket had access to employer-sponsored medical plans in March 2022, compared to 96% of workers in the highest-wage tier (BLS). This gap has direct implications for plan design strategy: organizations that extend affordable group health benefits across all pay bands — not just managerial or salaried roles — demonstrate measurable workforce equity and strengthen their position in competitive labor markets.

Sources Used

-

1

U.S. Bureau of Labor Statistics

In March 2022, only 26% of private industry workers in the lowest 10% wage bracket had access to employer-sponsored medical plans, compared to 96% of workers in the highest wage tier.

bls.gov/opub/ted/2023/coverage-in-employer-medical-care-plans-among-workers-in-different-wage-groups-in-2022.htm -

2

U.S. Internal Revenue Service

The ACA requires employers to report the cost of employer-sponsored group health plan coverage on Form W-2; the employer's contribution to premiums remains excludable from the employee's taxable income.

irs.gov/affordable-care-act/form-w-2-reporting-of-employer-sponsored-health-coverage -

3

U.S. Department of Labor — Employee Benefits Security Administration

Most employer-sponsored private-sector welfare plans offering health benefits are required to file a Form 5500 Annual Return/Report with the DOL.

dol.gov/agencies/ebsa/researchers/data/group-health-plan-data

Technology in Group Health Insurance

Core Technology Platforms & Systems

Benefits administration systems serve as the operational backbone, enabling HR teams to manage plan elections, dependent eligibility, premium calculations, and carrier data feeds from a single environment. These platforms integrate directly with payroll systems to ensure accurate deductions. Carrier portals — provided by insurers and third-party administrators — give employers real-time access to enrollment data, claims reporting, and plan utilization metrics.

Workflow Automation & Process Optimization

Automation has substantially reduced the manual burden of group health insurance administration. Open enrollment — historically a paper-intensive, error-prone cycle — is now managed through digital election workflows, and real-time confirmation notices without HR intervention. Qualifying life events, dependent verification, and COBRA notification are commonly handled through rules-based workflows.

Document & Data Management

Compliance documentation in group health insurance is substantial. Summary Plan Descriptions, Summary of Benefits and Coverage documents, Form 5500 filings, and HIPAA-governed plan records must be stored, versioned, and retrievable on demand. Cloud-based document management repositories with role-based access allow HR and legal teams to maintain audit-ready records. Electronic signature platforms and secure employee portals enable self-service access to plan documents year-round. Data retention policies must align with ERISA's six-year record-keeping requirement for plan documents and related filings.

AI & Emerging Technologies

Artificial intelligence is reshaping group health benefits. Intelligent document processing accelerates the extraction and validation of data from carrier invoices and enrollment confirmations, replacing manual reconciliation with automated exception flagging.

Integration & Interoperability

The group health insurance technology ecosystem spans benefits platforms, payroll systems, carrier data feeds, and HRIS environments — each historically operating as a data silo. APIs enables bidirectional, real-time data exchange. A common scenario: an employee's termination recorded in the HRIS automatically triggers a COBRA notification workflow and updates the carrier enrollment file — with no manual HR touchpoint required.

Skills & Adoption

Benefit professionals today need functional fluency in benefits administration platforms, data validation, and workflow configuration — not just regulatory knowledge. Successful rollouts typically pair system deployments with role-specific training, internal champions, and clear documentation of process changes to ensure consistent adoption across HR, payroll, and finance functions.

Key Performance Indicators (KPIs)

Group health insurance represents one of the largest and most complex line items in an organization's total compensation budget. Without disciplined KPI tracking, plan sponsors operate reactively — responding to cost spikes and enrollment errors after they occur rather than preventing them. Structured measurement connects benefits decisions to workforce strategy, giving HR, finance, and executive leadership a shared, evidence-based framework for plan design, vendor accountability, and annual renewal negotiations.

Core Operational KPIs

| KPI | Formula / Definition | Target |

|---|---|---|

| Enrollment Accuracy Rate | Correct enrollments ÷ Total enrollments processed | 99%+ |

| Open Enrollment Completion Rate | Employees completing elections ÷ Eligible employees | 100% within window |

| Dependent Eligibility Audit Pass Rate | Verified eligible dependents ÷ Total enrolled dependents | <3% ineligible rate |

| Average Time to Benefits Effective Date | Days elapsed from hire/QLE to confirmed active coverage | Minimize; no coverage gaps |

| COBRA Election & Payment Compliance Rate | Timely notices issued & payments processed ÷ Total qualifying events | 100% (statutory requirement) |

Financial & Cost-Efficiency KPIs

| KPI | Formula / Definition | Target |

|---|---|---|

| Per-Employee-Per-Month (PEPM) Cost | Total plan cost ÷ Covered employees ÷ 12 | Flat or declining YoY trend compared to inflation |

| Employer-to-Employee Premium Contribution Ratio | Employer premium share ÷ Total premium | 70–80% (employee-only); 50–65% (dependent tiers) |

| Medical Loss Ratio (MLR) | Claims paid ÷ Premiums collected | 80–85% minimum (ACA mandate for fully insured) |

Quality, Satisfaction & Emerging KPIs

| KPI | Description | Target |

|---|---|---|

| Employee Benefits Satisfaction Score | Collected via annual engagement or benefits-specific surveys; scores below 70% correlate with elevated voluntary turnover | 70%+ favorable |

| Benefits Inquiry Resolution Time | Average time from employee inquiry submission to resolution by HR or TPA | Under 48 hours |

| Carrier SLA Compliance Rate | Insurer/TPA adherence to contractual service levels for claims, ID cards, and dispute resolution | Per contract terms |

| Digital Self-Service Adoption Rate | Enrollment transactions & inquiries completed via self-service portal vs. HR-assisted channels | Increasing YoY; technology ROI indicator |

| Preventive Care Utilization Rate | Percentage of covered employees using in-network preventive services annually; leading indicator of long-term claims cost trajectory | Increasing YoY |

Measurement & Reporting Best Practices

Group health insurance KPIs should be reviewed on three cadences: monthly for operational metrics such as enrollment accuracy and inquiry resolution time, quarterly for financial metrics including PEPM trend and MLR, and annually for satisfaction and audit-based metrics tied to plan renewal decisions. Dashboards should present actuals against targets with year-over-year trend lines, distributed to HR leadership, finance, and senior plan committee members. Data should feed directly from the benefits administration system and carrier reporting portals to minimize manual aggregation error and ensure decisions rest on accurate, current information.

Frequently Asked Questions

What Is Group Health Insurance and How Does It Work?

Group health insurance is an employer-sponsored health coverage plan that insures a defined group of individuals — typically employees and their eligible dependents — under a single policy, with premiums shared between the employer and plan participants. Unlike individual market coverage, group plans pool risk across the entire enrolled population, which generally results in lower per-person premiums and broader access to benefits regardless of an individual's health history.

Employers select a plan structure — such as a Health Maintenance Organization (HMO), Preferred Provider Organization (PPO), or High-Deductible Health Plan (HDHP) — and negotiate terms with an insurer or third-party administrator. Employees then elect coverage during an annual open enrollment period or upon a qualifying life event such as marriage, the birth of a child, or loss of other coverage. Coverage typically extends to medical, dental, vision, and prescription drug benefits, though the specific components vary by employer design and budget.

What Is the Difference Between Fully Insured and Self-Funded Group Health Insurance?

Fully insured group health insurance transfers financial risk to the insurance carrier in exchange for fixed monthly premiums, while self-funded plans have the employer directly assume responsibility for paying employee claims. In a fully insured arrangement, the employer pays a set premium to the carrier regardless of how many claims employees file that month. The carrier absorbs the risk of high-cost claims and manages all claims processing — a model common among small and mid-size employers due to its cost predictability and administrative simplicity. In a self-funded (self-insured) plan, the employer pays claims as they occur using plan assets, typically with a stop-loss insurance policy in place to cap exposure. According to the 2024 KFF Employer Health Benefits Survey, 63% of covered workers nationally are enrolled in self-funded arrangements, rising to 79% among employees at large firms. Self-funding offers greater plan design flexibility and potential cost savings in low utilization years but introduces financial volatility that smaller employers may not be positioned to absorb. Choosing between these models requires detailed analysis of workforce size, claims history, risk tolerance, and administrative capacity.

Who Is Required to Offer Group Health Insurance Under Federal Law?

Employers with 50 or more full-time equivalent employees (FTEs) are required under the Affordable Care Act (ACA) to offer minimum essential, minimum value health coverage to their full-time workforce or face tax penalties. This provision — the Employer Shared Responsibility requirement under IRC Sections 4980H(a) and (b) — applies to organizations classified as Applicable Large Employers (ALEs). The ACA defines full-time employees as those working 30 or more hours per week on average. Employers with fewer than 50 FTEs are not subject to the mandate, though many choose to offer group coverage to remain competitive. Regardless of size, all employers offering group health plans must comply with ERISA reporting requirements, COBRA continuation coverage rules, and HIPAA privacy and portability standards.

How Are Group Health Insurance Premiums Calculated?

Group health insurance premiums are calculated based on a combination of plan type, coverage tier, geographic location, workforce demographics, and — for smaller employers — claims experience. Insurers use community rating or experience rating to set premium levels. Under community rating, required by the ACA for small group plans, premiums can only vary based on age, family size, geography, and tobacco use. Larger employers are typically subject to experience ratings, where historical claims data directly influence renewal pricing. Premiums are divided into coverage tiers: employee only, employee plus spouse, employee plus children, and family. According to the 2024 KFF Employer Health Benefits Survey, average annual premiums reached $8,951 for single coverage and $25,572 for family coverage. Employers typically absorb 70–80% of the single coverage premium, with employees paying the remainder through pre-tax payroll deductions governed by IRS Section 125 cafeteria plan rules. HR and finance teams use per-employee-per-month (PEPM) cost tracking to benchmark plan cost efficiency against industry peers year over year.

What Happens to Group Health Insurance When an Employee Loses Their Job?

When an employee loses job-based health coverage due to termination, reduction in hours, or other qualifying events, they are entitled under federal law to continue their group coverage temporarily through COBRA continuation coverage. The Consolidated Omnibus Budget Reconciliation Act (COBRA) requires employers with 20 or more employees to offer qualified beneficiaries — including the former employee, a spouse, and dependent children — the option to maintain their existing group health plan for up to 18 months, or up to 36 months in certain qualifying circumstances such as divorce or the death of the covered employee. The individual assumes full responsibility for the premium, including the employer's prior share, plus an administrative fee of up to 2%. Employers must issue a COBRA election notice within 14 days of the plan administrator receiving notice of a qualifying event. Non-compliance carries statutory penalties of up to $110 per day per qualified beneficiary. Employees who do not elect COBRA, or whose COBRA coverage expires, may qualify for a Special Enrollment Period through the ACA Marketplace — making the transition period a critical HR communication point.

Why Is Group Health Insurance Important to a Business's Competitive Position?

Group health insurance is the single most impactful employee benefit an organization can offer, directly influencing its ability to attract, retain, and sustain a productive workforce. Research consistently demonstrates that health benefits rank at or near the top of factors employees consider when evaluating job offers and deciding whether to remain with an employer. A workforce with access to quality group medical coverage experiences lower rates of absenteeism, earlier intervention on chronic conditions, and reduced presenteeism — the productivity loss associated with employees working while ill. From a total compensation benchmarking perspective, employers who fail to offer competitive group health benefits face a structural disadvantage in recruitment, particularly in industries where skilled labor is scarce. The IRS tax exclusion on employer premium contributions also means that every dollar invested in group health insurance delivers greater net value to employees than an equivalent dollar in taxable wages — making it one of the most cost-efficient levers in a compensation strategy. Organizations that treat group health insurance as a strategic asset consistently outperform peers in retention metrics and employer brand strength.

Key Takeaways

Group health insurance is far more than a line item on a benefits budget — it is a legally regulated, strategically significant component of how organizations attract talent, protect their workforce, and manage long-term cost exposure. Whether structured as a fully insured or self-funded plan, administered through an HMO, PPO, or HDHP model, or governed by ACA employer mandates and ERISA reporting requirements, effective group health plan management demands both regulatory fluency and strategic intent.

HR and benefits professionals who understand the financial mechanics, compliance obligations, and workforce impact of group health insurance are positioned to drive measurable organizational value well beyond the annual open enrollment window. As plan costs continue to rise and workforce expectations evolve, organizations that invest in thoughtful, data-informed plan design will hold a lasting competitive advantage.