Experience Modifier: Workers' Comp

What Is an Experience Modifier?

An Experience Modifier (also called an "e-mod" or "mod rate") is a numerical factor applied to a company's workers' compensation insurance premium, calculated by comparing its actual claims history against the expected losses for businesses of similar size and industry. It encompasses historical claim frequency and severity, payroll data, and industry benchmarks set by rating bureaus such as NCCI. Organizations with a mod below 1.0 receive premium discounts, while those above 1.0 pay surcharges — making it a financial incentive to invest in workplace safety and claims management.

Core Components

- E-Mod Calculation: The mod is calculated by dividing a company's actual losses by its expected losses, based on payroll size and industry classification, then applying a weighting formula set by the applicable rating bureau.

- Experience Period: The calculation uses three years of loss data, excluding the most recent completed policy year, producing a rolling three-year window that updates annually.

- Primary vs. Excess Losses: Claims are split into primary losses (the first portion of each claim, weighted heavily) and excess losses (amounts above the split point, weighted less). Frequency impacts the mod more than a single large claim.

- Expected Losses: Rating bureaus assign expected loss rates by industry classification code; payroll amount determines the total expected losses against which actual performance is measured.

Overview of Related Topics

- Rating Bureaus and Jurisdiction: NCCI administers the e-mod calculation in most U.S. states; a handful of states — including California, Michigan, and Pennsylvania — operate independent bureaus with their own rules and split-point thresholds.

- Financial Impact on Premiums: A mod of 1.0 is neutral; each point above or below applies to a corresponding percentage surcharge or credit directly to the workers' compensation premium, with high-claim employers sometimes carrying mods above 1.5.

- Eligibility Thresholds: Not all employers receive a mod — businesses must meet a minimum premium or payroll threshold (set by the applicable bureau) before experience rating applies.

- Claims Management Strategies: Reducing claim frequency, closing claims quickly, and implementing return-to-work programs are the primary levers employers use to lower their mod over the three-year experience period.

Key Topics in Experience Modifier Management

Rating Bureaus and Jurisdiction

- NCCI States: The National Council on Compensation Insurance governs e-mod calculations in approximately thirty-six states, standardizing split points, weighting values, and eligibility thresholds across these jurisdictions.

- Independent Bureau States: California (WCIRB), Michigan (DIFS), and a small number of others calculate mods using their own methodologies, which may differ in split-point amounts, ballast values, and minimum eligibility criteria.

Financial Impact on Premiums

- Premium Multiplier: The e-mod is multiplied directly against the manual premium (base rate × payroll), meaning a mod of 1.20 increases premium costs by 20% while a mod of 0.85 reduces them by 15%.

- Compounding Effect: Because the mod affects every classification on the policy, even modest increases compound across large payrolls — making a 0.10 mod improvement financially significant for mid-size and large employers.

Eligibility Thresholds

- Minimum Premium Requirement: Employers typically must generate a minimum average annual premium — often around $3,000–$10,000 depending on the bureau — before they are eligible for experience rating.

- New Employer Status: Companies without sufficient years of loss history are assigned a mod of 1.0 by default until they accumulate enough data to enter the experience rating program.

Claims Management Strategies

- Return-to-Work Programs: Structured transitional duty programs reduce lost-time claim severity, directly lowering the primary loss values that carry the greatest weight in the mod formula.

- Reserves Monitoring: Open claim reserves count in the mod calculation even before final settlement; working with carriers to ensure accurate — not inflated — reserves prevent artificial mod increases.

- Safety Program Investment: OSHA-compliant safety programs, hazard assessments, and employee training reduce claim frequency, which the mod formula penalizes more heavily than individual large losses.

A Closer Look at How the Experience Modifier Works

The Experience Modifier is a calculated numerical factor that directly determines how much an organization pays for workers' compensation insurance. Derived from three years of actual claims history compared against expected losses for businesses of similar size and industry classification, it reflects how well a company manages workplace safety and employee wellbeing. Rating bureaus such as NCCI assign the workers' compensation mod annually, and it functions as both a financial benchmark and an operational signal. Organizations with strong safety records earn e-mod rates below 1.0, receiving premium credits, while those with elevated claims histories pay surcharges proportional to their risk exposure.

HR professionals, risk managers, and finance leaders all rely on the Experience Modifier to make sound decisions about insurance budgeting, safety program investment, and claims management. Brokers and carriers use it to price workers' compensation coverage, while internal teams track it as a performance indicator for occupational health and loss control programs. A low e-mod rate reflects consistent organizational focus on reducing claim frequency and severity through return-to-work programs, hazard assessments, and employee training. For HR teams, actively managing the workers' compensation mod translates directly into lower operating costs and stronger workplace safety outcomes.

Key Infographic Statistics at a Glance

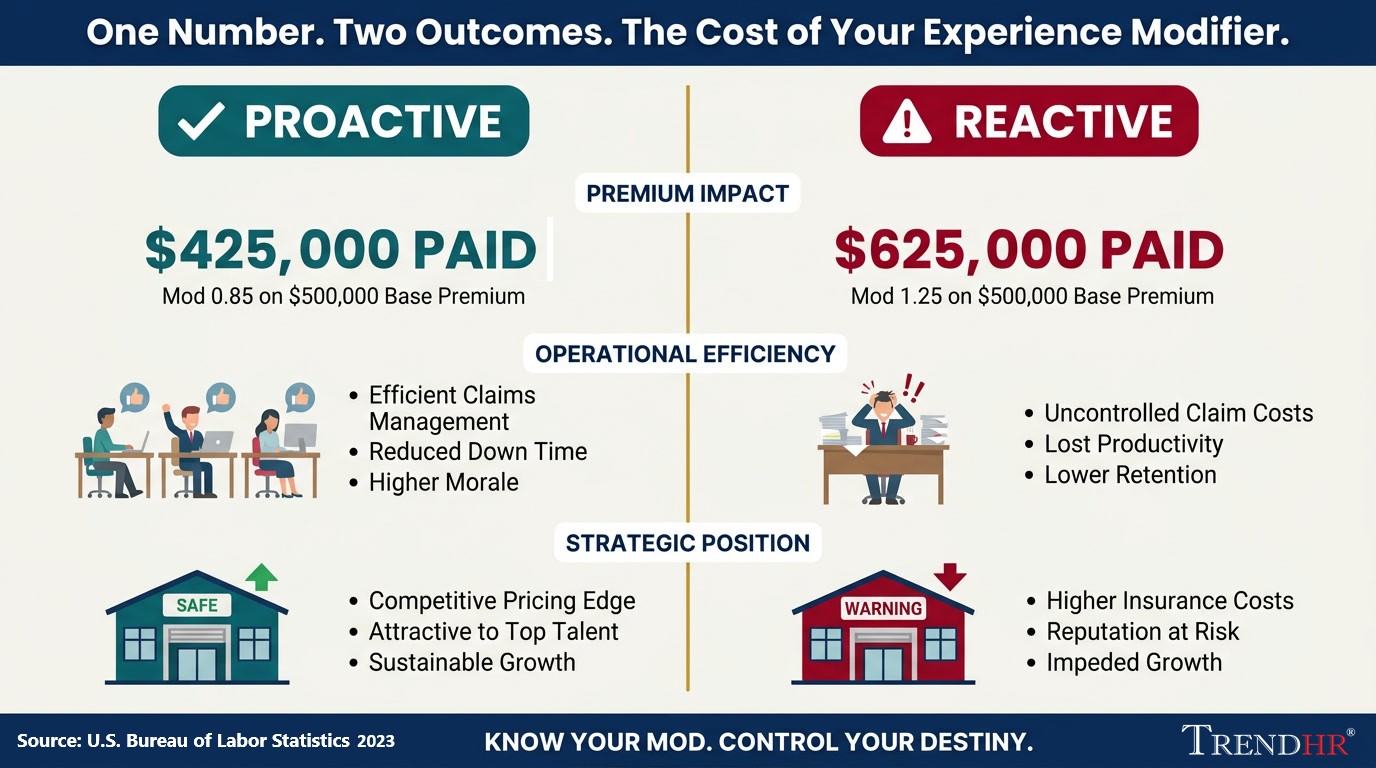

- $175,000 — annual premium variance between 0.85 mod and a 1.20 mod on a $500,000 base premium

- $0.46 per hour — average workers' comp cost per employee (BLS, 2022), making even small mod changes consequential at scale

- 15 states trigger mandatory written safety program requirements for employers with mods between 1.2–2.0

- 3-year rolling window — how long loss history is tracked, meaning improvement takes time but decay does too

- 0.80–0.90 — the mod range risk professionals consider "strong" for an active mid-size employer

The Experience Modifier is one of the most financially significant and controllable variables in workers' comp — organizations that actively manage it save real money and reduce regulatory exposure; those that ignore it face compounding costs.

Statistics and Outlook

How Is an Experience Modifier Calculated?

The Experience Modifier is calculated by dividing a company's actual losses by its expected losses, then applying a weighting formula that emphasizes claim frequency over individual claim size. Expected losses are derived from an employer's payroll amount and industry classification codes, with each code carrying a predetermined expected loss rate set by the applicable rating bureau.

The calculation uses a three-year experience period — typically the three policy years before the most recently completed year. Each year's losses are split into primary losses (the first portion of each claim, weighted heavily) and excess losses (amounts above the split point, weighted less). This structure ensures that a company filing many small claims is penalized more than one experiencing a single catastrophic event of equivalent dollar value.

One commonly misunderstood aspect of the mod is that open claims count. Reserve amounts on unresolved claims are included in the calculation even before final settlement. An inflated reserve on a single open claim can temporarily push a mod higher than a company's actual claims experience warrants, which is why proactive reserve monitoring and carrier communication are essential practices.

The resulting mod is expressed as a decimal — for example, 0.82 (meaning an 18% premium discount) or 1.35 (meaning a 35% surcharge). For an employer paying $500,000 in base workers' compensation premium, the difference between a 0.85 mod and a 1.20 mod represents $175,000 in annual premium variance — a figure that underscores why mod management belongs on the CFO's radar alongside HR's.

What Is a Good Experience Modifier Rate?

A good Experience Modifier is any value below 1.0, which indicates that a company's claims history is better than the expected average for its industry and size. The lower the mod, the greater the premium discount and the stronger the organization's demonstrated safety performance.

Most risk management professionals consider a mod in the 0.80–0.90 range to be a strong result for a mid-size employer with active safety programs. Achieving a mod below 0.75 typically requires several consecutive years of low claim frequency, disciplined return-to-work practices, and rigorous claims management — and is more common among large employers with the resources to invest systematically in loss control.

A mod of exactly 1.0 is not a failure — it simply means the company's performance matches the industry baseline. However, it does represent a missed opportunity for premium savings and signals that safety and claims practices are average at best.

Mods above 1.0 warrant immediate attention. OSHA research identifies employers with experience modification rates ranging from 1.2 to 2.0 as candidates for mandatory written safety program requirements in at least 15 states, meaning a high mod can trigger regulatory consequences beyond just elevated premiums. Some public sector contracts and construction bids also impose hard mod caps — commonly 1.0 or 1.25 — disqualifying employers with poor safety records from competing entirely.

The practical implication: a "good" mod is one that trends downward over time, reflecting continuous improvement in workplace safety and claims outcomes.

How Can a Company Lower Its Experience Modifier?

A company can lower its Experience Modifier by reducing the frequency of workplace injuries, closing claims quickly and cost-effectively, and implementing a structured return-to-work program that minimizes lost-time costs. Because the mod formula penalizes frequency more heavily than severity, preventing multiple small claims does more to improve the mod than managing a single large one.

The most impactful strategies fall into three categories:

Safety Program Investment — OSHA's research consistently links formal safety and health programs to measurable reductions in injury rates. Hazard assessments, employee training, and supervisor accountability structures all reduce claim frequency, which is the variable most directly tied to mod improvement.

Claims Management — When injuries do occur, how a company responds matters significantly. Prompt reporting, proactive communication with the injured employee, and regular reserve reviews with the carrier all reduce both claim cost and duration. Disputed or mismanaged claims tend to remain open longer, keeping reserve amounts in the mod calculation.

Return-to-Work Programs — Modified duty assignments allow injured employees to return to productive work before they have fully recovered, reducing lost-time claim severity. Because excess losses are down-weighted in the mod formula, cutting the duration of lost-time claims has a meaningful impact on the primary loss figures that drive the calculation.

Because the mod reflects a rolling three-year window, improvement takes time to appear in the rate. Companies that begin investing in safety and claims management today should expect to see meaningful mod reduction within two to three annual renewal cycles.

Understanding Modifier

According to the U.S. Bureau of Labor Statistics, workers' compensation costs averaged $0.46 per employee hour worked across all civilian workers as of December 2022 — approximately 1% of total compensation — making even modest modifier changes financially consequential at scale. Understanding the Experience Modifier is increasingly important given the volume of workplace claims driving it. The BLS reports that private industry employers recorded 2.5 million nonfatal workplace injuries and illnesses in 2024, at a rate of 2.3 cases per 100 full-time equivalent workers. Regulatorily, the stakes extend beyond insurance costs: OSHA research identifies above-average workers' compensation experience modification rates — generally ranging from 1.2 to 2.0 — as a criterion triggering mandatory safety program requirements in at least 15 states. Organizations that actively manage their claims frequency, invest in return-to-work programs, and monitor open reserves are best positioned to drive their modifier below 1.0 — reducing premium costs while building a measurable safety culture.

Sources Used

-

1

U.S. Bureau of Labor Statistics — Monthly Labor Review

Workers' compensation averaged $0.46 per employee hour worked across all civilian workers as of December 2022, approximately 1% of total compensation.

bls.gov/opub/mlr/2023/article/removing-workers-compensation-costs-from-the-national-compensation-survey.htm -

2

U.S. Bureau of Labor Statistics — Injuries, Illnesses, and Fatalities Program

Private industry employers reported 2.5 million injury and illness cases in 2024, with a total recordable case rate of 2.3 per 100 full-time equivalent workers.

bls.gov/iif -

3

OSHA — Injury and Illness Prevention Programs White Paper

15 states specifically target employers with above-average workers' compensation experience modification rates (ranging from 1.2 to 2.0) for mandatory written safety programs.

osha.gov/sites/default/files/OSHAwhite-paper-january2012sm.pdf

Technology in Experience Modifier Management

Core Technology Platforms & Systems

Managing an organization's Experience Modifier requires coordinating across several interconnected technology categories. Workers' compensation management platforms serve as the operational hub, tracking claims from first report of injury through closure while feeding loss data into premium calculations. These systems integrate with broader human resource information systems that maintain payroll records — a critical input, since payroll by classification code directly determines expected losses and mod eligibility thresholds. Insurance agency management systems used by brokers and carriers house policy history, prior mod worksheets, and premium audit records. Together, these platforms give risk managers, HR leaders, and finance teams a view of the variables driving their organization's mod.

Workflow Automation & Process Optimization

Automation is reducing the manual effort required to manage mod-related workflows. Software now handles routine tasks such as extracting loss run data from carrier portals, populating mod worksheets, and flagging discrepancies between actual and expected loss figures. Workflows route first reports of injury through approval chains, notify supervisors of open claims, and trigger return-to-work plan templates. APIs synchronize payroll data across systems on a scheduled basis, ensuring that classification codes and hours-worked figures remain current.

Document & Data Management

Experience Modifier management generates substantial documentation: loss runs, mod worksheets, payroll audit records, claims files, and dispute correspondence. Cloud-based document repositories with role-based access controls allow HR, risk, legal, and finance teams to retrieve relevant records without duplicating files. Electronic signature platforms streamline audit acknowledgments and carrier correspondence. Because workers' compensation records intersect with OSHA recordkeeping requirements under 29 CFR Part 1904, document retention policies must account for both insurance and regulatory timelines — typically five years for OSHA logs and up to seven years for claims-related records depending on jurisdiction.

AI & Emerging Technologies

AI models trained on historical claims data can identify employees or job classifications at elevated injury risk, allowing targeted safety interventions before claims materialize and affect the mod. Intelligent document processing extracts structured data from unstructured loss runs and medical reports, reducing manual data entry. Natural language processing tools assist risk managers in reviewing claim narratives for subrogation opportunities or reserve accuracy concerns. AI-driven reserve adequacy tools are positioned to give employers earlier visibility into claims that could affect future mod calculations.

Integration & Interoperability

Data silos between HR, payroll, safety, and claims systems remain the primary obstacle to accurate mod management. When payroll classification data in an HRIS does not match the figures submitted during a workers' compensation audit, mod errors result — often unfavorably. Organizations that establish a unified data ecosystem see measurable improvements in mod accuracy, premium audit outcomes, and claims reserve monitoring.

Skills & Adoption

Risk managers and HR professionals need to coordinate claims data interpretation, workers' compensation rating methodology, and the reporting capabilities of their carrier and broker platforms. Common adoption barriers include departmental ownership disputes over claims data and inconsistent payroll classification practices. Successful implementations pair technical onboarding with cross-functional training, ensuring that HR, finance, and operations teams understand how their data inputs directly affect the organization's mod — and its insurance costs.

Key Performance Indicators (KPIs)

Tracking KPIs in Experience Modifier management transforms a reactive insurance function into a proactive business discipline. Because the mod is a lagging indicator — reflecting claims activity from the prior three years — organizations that wait until renewal to assess their performance have already missed their window to influence the outcome. Structured KPI monitoring creates feedback loops that connect daily safety decisions to long-term premium costs, enabling HR, risk, and finance leaders to intervene early and hold operations accountable for results.

Experience Modifier KPIs should be reviewed on three cadences: monthly for operational metrics like TRIR, LTIR, and open claim counts; quarterly for financial metrics including cost-per-claim and mod-driven premium variance; and annually for mod accuracy review and benchmark comparison. A well-structured dashboard surfaces these metrics side by side, making the connection between safety performance and insurance cost visible to every stakeholder — from frontline supervisors to the executive team.

Core Operational KPIs

| KPI | Formula | Target |

|---|---|---|

| Current Experience Modifier | Actual losses ÷ Expected losses (bureau weighting applied) | 0.75–0.90 (best-in-class) |

| Total Recordable Incident Rate (TRIR) | (Recordable incidents × 200,000) ÷ Total hours worked | Below NAICS industry benchmark |

| Lost Time Incident Rate (LTIR) | (Lost-time cases × 200,000) ÷ Total hours worked | Below NAICS industry benchmark |

| Claims Frequency Rate | WC claims filed ÷ (Employees ÷ 100) | Consistent downward trend YoY |

| Average Claim Duration | Total lost workdays ÷ Number of lost-time claims | Below industry peer average |

| Return-to-Work Rate | Employees returned within 30 days ÷ Total injured employees × 100 | >80% |

Financial & Cost-Efficiency KPIs

| KPI | Formula | Target |

|---|---|---|

| WC Premium as % of Payroll | WC Premium ÷ Total Payroll × 100 | Consistent year-over-year reduction |

| Cost Per Claim | Total claim costs (medical + indemnity) ÷ Number of claims | At or below industry peer group average |

| Mod-Driven Premium Variance | (Actual mod − 1.0) × Base manual premium | Negative value (premium credit) or minimized surcharge |

Quality, Compliance & Forward-Looking KPIs

| KPI | Description | Target |

|---|---|---|

| Mod Accuracy Rate | Percentage of annual mod worksheets reviewed and confirmed free of bureau calculation errors | 100% review completion; errors corrected before renewal |

| Claims Reopening Rate | Percentage of closed claims that reopen within 12 months, signaling inadequate medical resolution | <5% |

| Safety Audit Compliance Score | Completion rates and findings from scheduled workplace safety audits; a leading indicator of future claim activity | 100% completion; zero critical findings |

| Return-to-Work Program ROI | Premium savings attributable to reduced lost-time claim severity relative to program operating costs | Positive ROI; typically 3:1 or better |

Frequently Asked Questions

What Is an Experience Modifier in Workers' Compensation?

An Experience Modifier (also called an e-mod, mod rate, or experience modification factor) is a numerical multiplier applied to a company's workers' compensation insurance premium based on its actual claims history compared to industry peers. A mod of 1.0 is neutral — it represents average performance for businesses of similar size and classification. Employers with fewer or less severe claims than average earn a mod below 1.0 and pay reduced premiums; those with worse-than-average claims histories receive a mod above 1.0 and pay surcharges.

The Experience Modifier is calculated annually by a rating bureau — most commonly the National Council on Compensation Insurance (NCCI) — using three years of loss data, excluding the most recently completed policy year. The formula weighs both claim frequency and severity, though frequency carries heavier weight. This means a company with several small claims will typically see a higher mod than one with a single large claim of equal total cost. For most mid-size and large employers, the mod is one of the most controllable variables in their workers' compensation spend.

How Is an Experience Modifier Calculated?

The Experience Modifier is calculated by dividing a company's actual losses by its expected losses, then applying a weighting formula that emphasizes claim frequency over individual claim size. Expected losses are derived from an employer's payroll volume and industry classification codes, with each code carrying a predetermined expected loss rate set by the applicable rating bureau. The calculation uses a three-year experience period — typically the three policy years before the most recently completed year — and splits each year's losses into primary losses (heavily weighted) and excess losses (less weighted). Open claim reserves are included even before final settlement, making proactive reserve monitoring essential to preventing artificially inflated mods.

What Is a Good Experience Modifier Rate?

Any mod below 1.0 is favorable, indicating better-than-average claims performance for the employer's industry and size. Most risk management professionals consider a mod in the 0.80–0.90 range to be strong for a mid-size employer with active safety programs. A mod of exactly 1.0 is not a failure, but it signals average performance and a missed opportunity for premium savings. Mods above 1.0 — particularly in the 1.2–2.0 range — can trigger regulatory consequences such as mandatory written safety program requirements in at least 15 states and may disqualify employers from public contracts or construction bids with hard mod caps.

How Can a Company Lower Its Experience Modifier?

A company can lower its Experience Modifier by reducing injury frequency, closing claims quickly, and implementing structured return-to-work programs. Because the mod formula penalizes claim frequency more heavily than severity, preventing multiple small claims is more impactful than managing a single large one. Key strategies include investing in OSHA-compliant safety programs and employee training, monitoring open claim reserves with the carrier to prevent inflation, and providing modified duty assignments to injured workers to reduce lost-time claim severity. Because the mod reflects a rolling three-year window, organizations should expect meaningful improvement within two to three annual renewal cycles after implementing consistent safety and claims management practices.

Who Is Responsible for Managing the Experience Modifier?

Managing the Experience Modifier is a shared responsibility across HR, risk management, finance, and operations — with no single department holding full control over every variable that drives it. In practice, the lead owner varies by organization size and structure.

In smaller companies, the HR manager or business owner typically manages the mod with guidance from a workers' compensation broker. In mid-size organizations, a risk manager or Director of HR usually owns the function, coordinating with the carrier on claims strategy and with operations on safety programming. Large enterprises often employ dedicated risk management departments that monitor the mod continuously, model the financial impact of open claims, and engage third-party administrators (TPAs) to manage claims professionally.

The workers' compensation broker plays a central supporting role regardless of company size. A knowledgeable broker reviews the mod worksheet annually for calculation errors — which are more common than most employers realize — and helps clients understand which open claims are creating the most upward pressure on future mods. Mod disputes can be filed with the applicable rating bureau when data errors are identified, and successful disputes can result in retroactive premium adjustments.

Finance and operations leaders should be actively involved as well. Because the mod directly affects insurance premiums, it belongs in budget forecasting discussions. And because claim frequency is shaped by frontline working conditions, operations managers are often the most effective lever for prevention — making cross-functional ownership the most successful model.

Key Takeaways

The Experience Modifier is one of the most financially significant and operationally controllable variables in a company's workers' compensation program. It rewards organizations that invest in workplace safety, manage claims proactively, and monitor their loss data with discipline — and it penalizes those that don't with compounding premium surcharges. A mod below 1.0 represents real dollars saved; a mod trending upward signals systemic risk that extends beyond insurance costs into regulatory exposure and contract eligibility.

As predictive analytics and AI-driven claims tools become more accessible, forward-thinking organizations will increasingly be able to identify risk before claims occur — shifting mod management from a reactive financial exercise to a proactive driver of workforce health and business performance.